Take-up on the European office markets remained stable in 2025 and was thus at a comparable level in 2023 and 2024. This sideways movement confirms that the five-year average is the new benchmark after the pandemic. Both leasing and investment dynamics across Europe are characterised by a focus on high-quality assets and central locations. In addition to this clear polarization, market activity is characterized above all by the noticeable recovery in the investment market. With the stabilization of interest rates, interest in large-volume deals has recently risen again, which is a clear sign of the resurgent investor confidence in the European office markets. This is the result of the analysis by BNP Paribas Real Estate.

Stable take-up in 2025

After a lively and promising first half of the year, leasing activity in Europe slowed down in the second half of 2025. In the third quarter, a minus of 6% was registered, followed by minus 4% in the fourth quarter. Overall, total take-up in 2025 in the 18 leading European office markets[1] amounted to just over 8 million m². “This result is roughly the same as the previous two years and is close to the five-year average, which is now emerging as a new benchmark after the pandemic. In the CBD, momentum remains high, while decentralised locations with limited connectivity and weak infrastructure are increasingly facing challenges,” said Etienne Prongué, Head of the International Investment Group (IIG) at BNP Paribas Real Estate.

The good performance of some markets is remarkable, especially Frankfurt, where take-up rose by 54% year-on-year to 611,000 m² – the highest figure since 2019 and 31% above the five-year average. “This outstanding performance was driven by exceptional transactions, with the contracts of Commerzbank (73,000 m²) and ING-DiBa (32,400 m²), which were already successfully brokered by BNP Paribas Real Estate in the first quarter of 2025, giving the starting signal for a strong year,” explains Marcus Zorn. The next largest deal was made by KPMG (33,400 m²) in the second quarter.

London also recorded a significant increase in take-up (+11% compared to 2024), supported by strong market momentum in the King’s Cross (+35%) and Southbank (+16%) submarkets. Luxembourg and Dublin, which are typically more volatile due to their smaller market size, also performed well in 2025, recording gains of 34% and 14% respectively.

Growing offer with strong differences between locations

The overall vacancy rate in Europe stood at 9.5% at the end of 2025, an increase of 50 basis points year-on-year. Although the vacancy rate has generally increased due to a growing gap between supply and demand, trends vary greatly by location. In central locations, availability remains limited and is likely to fall even further, especially in the new-build segment, while vacancy rates are rising sharply in the outskirts and for outdated existing properties.

The average vacancy rate in the CBD was 5.6% at the end of 2025, compared to 11.1% in the decentralised locations. Since 2020, the vacancy trend in the central top locations and the less well-connected peripheral locations has diverged. The markets are increasingly divided into two parts. The most pronounced differences are in Barcelona, Paris and Brussels. For example, in Barcelona, the vacancy rate in the CBD is 1.6%, compared to over 12% in the secondary locations. “Hybrid forms of work as well as the renewed focus on communication and meeting colleagues in the office continue to drive user demand for space in established central locations. Accessibility remains just as important as the quality of the property,” explains Etienne Prongué.

Prime rents continue to rise

Prime rents have continued to rise in most European cities, supported by the ongoing shortage of premium space in the absolute top locations. The Southern European markets stood out in particular, with strong rental growth in Milan (+11%), Barcelona (+10%), Madrid (+6%) and Rome (+4%). “In the German office markets, too, the significant excess demand in the premium segment has led to a noticeable increase in prime rents in Germany’s top 5 locations. The increase was particularly extensive in Munich at 8%. At currently €58.00/m², Munich is now Germany’s most expensive office market. Düsseldorf rose by 6% to €46.00/m² and Hamburg to €38.00/m², with the first deals above €40/m² also registered in the Hanseatic city,” adds Marcus Zorn, CEO of BNP Paribas Real Estate Germany. On average, prime rents rose by 4.4% in around forty European markets in 2025.

Investments are picking up speed again

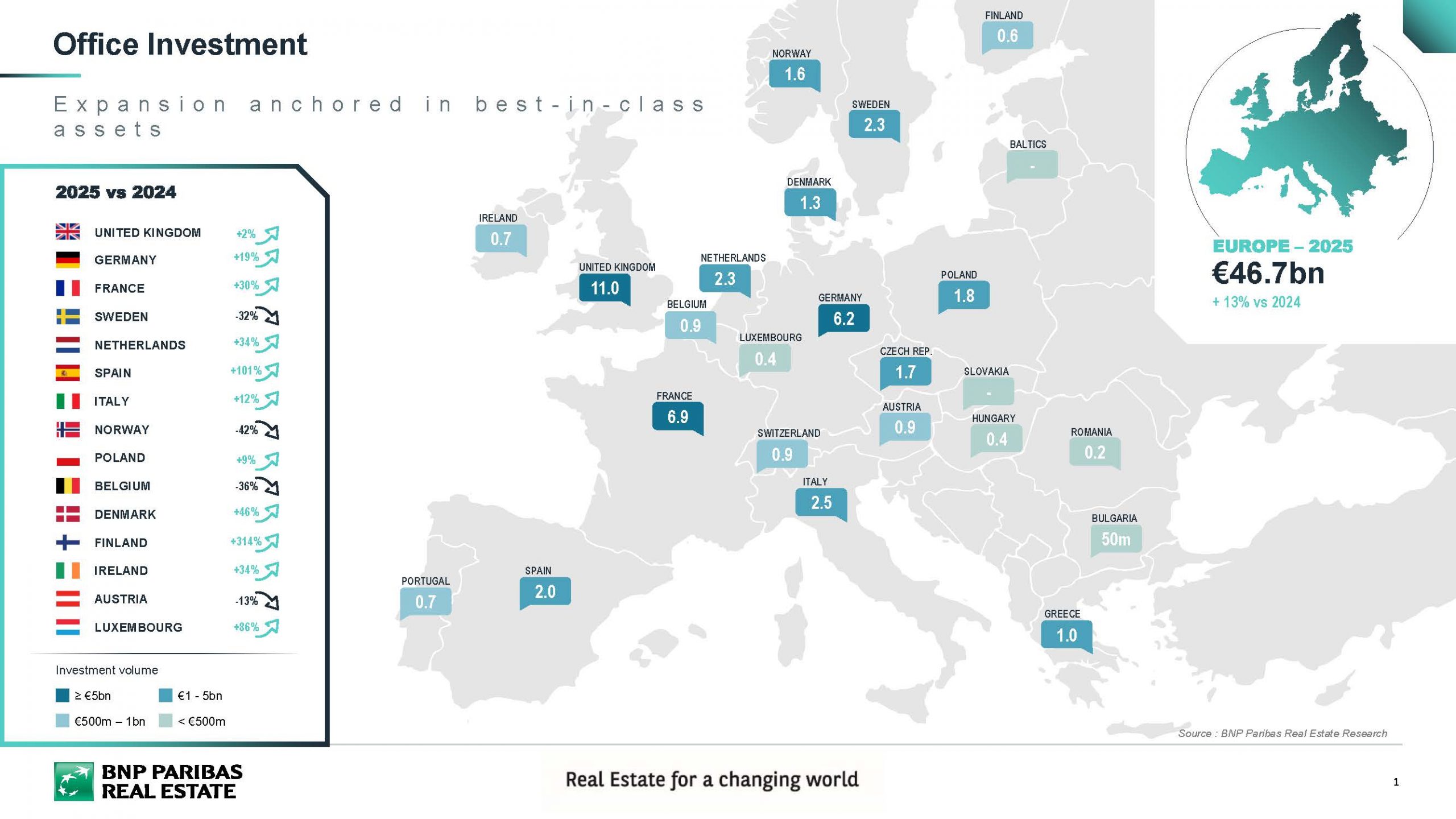

In 2025, the European commercial real estate investment market confirmed its upward trend at almost €177 billion, an increase of 9% compared to 2024. This growth reflects the general return of investors on the one hand, but also their more targeted and selective investment strategies compared to pre-crisis comparisons. “The office investment market has benefited from this development and is now once again the strongest asset class with an increase of 13% and an investment volume of € 47 billion achieved in 2025. This momentum was supported in particular by large-volume transactions in Europe’s main capitals,” says Etienne Prongué.

Highlights in the fourth quarter were the sale of the striking “Can of Ham” office tower (30,000 m²) in London and the sale of a 40,000 m² building on Avenue Kléber in Paris for more than €700 million. A slow market recovery was observed across Europe in 2025. In the United Kingdom, the volume of office investments accelerated slightly to €11 billion (+2%). The UK is thus by far the largest market, followed by France and Germany, which recorded strong growth in office investments of plus 30% to €6.9 billion and 19% to €6.2 billion respectively. Italy reported an increase of 12% to €2.5 billion and the Netherlands 34% to €2.3 billion. At a low level, the investment volume in Spain doubled to €2 billion compared to the previous year.

Prime yields stabilise – yield compression expected

The level of prime yields stabilised across countries in the second half of 2025. The inflation rate, which is within the target corridor of the European Central Bank, and the stable development of the key interest rate in the long term had a positive impact. The Bank of England’s more expansionary monetary policy is also supporting the momentum in the office investment market.

The past quarters have also confirmed the ongoing polarization in the office investment markets. While the price level has stabilised in the most sought-after locations and in the segment of top assets in Europe’s largest cities, price adjustments remain the order of the day, especially for old existing buildings in poorly connected locations.

“As can be seen in London and Paris, investor interest is returning to Europe’s capitals and top cities, supported by improved financing conditions. Transaction momentum in the UK, France and Germany is likely to pick up as early as the first half of 2025. Demand for core assets should keep the pressure on prime yields high,” says Etienne Prongué.