Energy

Renewable energies have been an economically and even more socially important asset class not only since the energy transition.

Top contribution

Renewable Energy Investments – News & Analysis for Investors | ASSETPHYSICS

Renewable Energy Investment – News, Market Analysis and Background Knowledge for Institutional Investors

This category brings together current news, specialist articles and market analyses on renewable energy investment as an institutional asset class. The content is aimed at pension funds, insurers, pension schemes, sovereign wealth funds, family offices and asset managers that view renewable energy as an independent component of their private markets or infrastructure allocation.

What is a Renewable Energy Investment? – Definition

A renewable energy investment refers to the investment of private or institutional capital in assets, projects and infrastructure for the generation, storage and transmission of energy from renewable sources. These include solar parks (photovoltaics), wind turbines (onshore and offshore), battery energy storage systems (BESS), hydrogen facilities, bioenergy and electricity grids for the integration of renewable generation.

As an institutional asset class, renewable energy investment belongs to the broader category of infrastructure investments and shares their structural characteristics: long-term, predictable cash flows, low correlation with public markets and a social indispensability that favours political support and regulatory protection. The key difference from traditional infrastructure lies in its growth potential: renewable energy is not just an existing market – it is the fastest-growing area of global capital allocation in the real assets segment.

Renewable energy investment can take the form of both equity and debt. On the equity side, there are direct stakes in project companies, fund units in specialised infrastructure funds and co-investments. On the debt side, there are project finance loans, green bonds and infrastructure debt funds. Many institutional investors combine both access routes.

Why Renewable Energy Investment Has Become a Central Topic for Institutional Portfolios

The importance of renewable energy investment for institutional investors has grown structurally in recent years – and this trend is lasting. Three factors explain this growth:

The first factor is the global investment requirement. Investment in the electricity sector is expected to reach USD 1.5 trillion in 2025 – around 50 percent more than total spending on oil, gas and coal combined. The full decarbonisation of the global economy requires investments of more than USD 100 trillion over the next three decades, a substantial share of which will take the form of equity for renewable energy. Public budgets cannot cover this demand alone – private institutional capital is structurally indispensable.

The second factor is rising electricity demand driven by digitalisation and artificial intelligence. Data centres for AI training and inference, electric mobility and the decarbonisation of industrial processes are driving electricity demand at a historically unprecedented pace. More than half of institutional investors worldwide cite new technologies and the resulting electricity demand as the megatrend with the strongest influence on their allocation decisions.

The third factor is the geopolitical reorganisation of energy supply. Dependence on fossil energy imports, made painfully visible during the 2022 energy crisis, has dramatically increased the political priority of energy security and domestic renewable generation. State support programmes and accelerated permitting procedures create the stable regulatory framework that institutional investors need for long-term capital allocation.

This is reflected in the fund landscape: renewable energy accounted for around two thirds of sector-specific capital allocations in global infrastructure funds in the first three quarters of 2025 – no other infrastructure segment comes close to this share.

The Most Important Segments in Renewable Energy Investment

Renewable energy investment is not a homogeneous asset class. The subsegments differ significantly in risk profile, regulatory framework, cash flow structure and capital requirements.

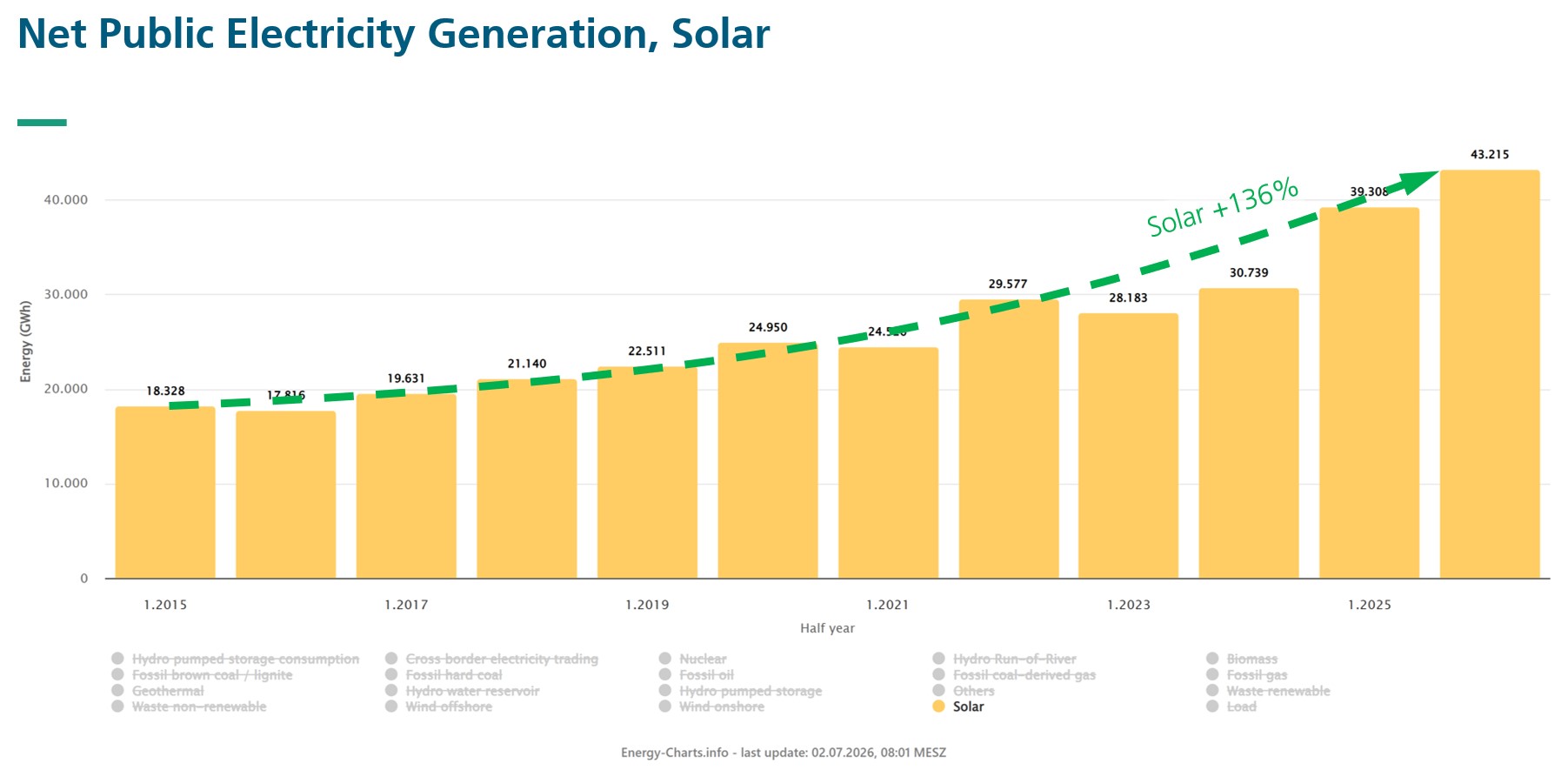

Solar energy (photovoltaics) is the fastest-growing segment by volume. Utility-scale solar parks offer institutional investors long-term, contractually secured cash flows through power purchase agreements (PPAs) or feed-in tariffs, with comparatively low operating risk. Falling technology costs, rising electricity demand and political support make solar the most accessible greenfield strategy in renewable energy investment. In Germany, photovoltaic expansion doubled in 2025 compared with the previous year to around 4.6 gigawatts.

Wind energy (onshore and offshore) offers higher capacity factors than solar and is suitable for very large investment volumes. Onshore wind has become significantly more attractive again in Germany due to simplified approval procedures. Offshore wind – particularly in the North Sea and Baltic Sea – is the most capital-intensive segment of renewable energy investment: individual projects reach several billion euros, financing structures require deep project finance expertise and specialised technical due diligence.

Battery storage systems (BESS) are the fastest-growing segment within renewable energy investment. Battery storage is currently undergoing a revolution, with investment three times as high as in 2021. It is system-critical for integrating volatile renewable generation and for grid stability. Cash flows arise from capacity markets, frequency regulation and arbitrage strategies – a complex but attractive risk profile for specialised energy investors.

Electricity grids and transmission infrastructure are the structural bottleneck of renewable energy investment. Without massive grid expansion, renewable energy cannot be fully integrated. Grid investments are highly regulated, and therefore offer very stable, predictable returns and long maturities – making them particularly attractive for core infrastructure allocations by pension funds and insurers.

Hydrogen and power-to-X are the strategic future segment of renewable energy investment with the greatest potential for decarbonising industrial processes that cannot be directly electrified. Green hydrogen is technically available, but not yet competitive. Institutional early investors are positioning themselves through specialised funds and state-supported pilot projects.

Power purchase agreements (PPAs) as a financing instrument form the structural foundation of modern renewable energy investment. A PPA is a long-term electricity offtake agreement between an energy producer – typically a solar or wind park – and an electricity buyer, guaranteeing a fixed or indexed electricity price over ten to twenty years. PPA-backed assets offer institutional investors predictable cash flows without direct dependence on state subsidies and are regarded as the preferred structuring format for subsidy-free renewable energy investments in Europe.

Renewable Energy Investment in Germany: Regulation, Market and Support Programmes

Germany is one of the most important markets for renewable energy investment in Europe – and is gaining in attractiveness due to changing framework conditions.

In the third quarter of 2025, renewable energy in Germany reached a new all-time high, accounting for 64.1 percent of domestic electricity generation. Wind and solar together delivered more than half of Germany’s electricity – a structural shift that makes the further expansion of storage, grids and flexible demand management essential, thereby creating new investment opportunities along the entire value chain of renewable energy investment.

The Location Promotion Act, which came into force at the end of 2025, significantly improves the regulatory framework for private renewable energy investments in Germany. Open-ended real estate funds will in future be allowed to invest up to 15 percent of their assets in renewable energy and related infrastructure. In addition, the German government has launched the Deutschlandfonds, which, through state guarantees of around EUR 30 billion, is intended to trigger total investments of around EUR 130 billion – a considerable part of it in the energy sector.

The Renewable Energy Sources Act remains the central regulatory framework for renewable energy investment in Germany. EEG-backed assets offer regulatorily supported cash flows and are considered core investments. Assets that have completed their EEG remuneration period must be financed through corporate PPAs or the market and therefore require deeper market expertise.

According to the KfW Climate Barometer, Germany must invest around EUR 5 trillion to achieve its legally defined target of climate neutrality by 2045 – an average of more than EUR 190 billion per year. This corresponds to around five percent of German gross domestic product and makes renewable energy investment one of the largest-volume investment fields in the German economy for the next two decades.

Opportunities and Risks in Renewable Energy Investment

Renewable energy investment offers institutional portfolios several structural advantages: long-term, often inflation-linked cash flows through PPAs or regulated remuneration; low correlation with public equity markets; a natural contribution to ESG goals and net-zero commitments; state support and incentive programmes as a regulatory safety net; and structurally growing demand driven by electrification, AI and decarbonisation.

The risks are real and must be carefully considered in portfolio construction. Regulatory risk is the central risk in renewable energy investment: changes to feed-in tariff regimes, altered grid fees or political intervention in remuneration schemes can place significant pressure on project returns. Resource risk – the possibility that wind or sun is weaker than modelled – is relevant for individual projects, but largely compensable in diversified portfolios. Technology risk particularly affects battery storage and hydrogen. Construction risk in greenfield projects is especially pronounced in offshore wind. And interest-rate risk: higher financing costs make project finance more expensive and weigh on valuations of long-duration cash flow assets.

Institutional investors’ return expectations for infrastructure equity rose to 13.4 percent net in 2025 – an increase of 200 basis points compared with the previous year. This reflects the increased risk appetite and improved return prospects in renewable energy investment.

Frequently Asked Questions About Renewable Energy Investment

What is meant by a renewable energy investment? A renewable energy investment refers to the investment of private or institutional capital in assets for the generation, storage or transmission of energy from renewable sources: solar energy, wind power, battery storage, hydrogen, bioenergy and electricity grids. As an institutional asset class, renewable energy investment is generally assigned to the infrastructure sleeve of a portfolio and offers long-term, predictable cash flows with low correlation to public markets.

What returns are realistic in renewable energy investment? Return ranges vary significantly depending on the segment and risk profile. Core-like assets (existing onshore wind turbines or solar parks with a long-term PPA) typically deliver five to eight percent IRR. Core-plus strategies (solar platforms, battery storage) target eight to twelve percent. Greenfield projects and speculative segments such as hydrogen may target twelve percent or more, with correspondingly higher risk. Infrastructure debt in renewable energy offers four to seven percent in the current interest-rate environment for senior secured financings.

How can institutional investors invest in renewable energy? The main access routes are: closed-ended infrastructure funds with an energy focus; special funds under KAGB or ELTIF 2.0 for cross-border structures; direct investments in project companies; co-investments alongside a fund GP; infrastructure debt for a more conservative risk positioning; and auction procedures as direct project access. Minimum ticket sizes vary widely – from a few million euros in fund participations to double-digit million amounts in direct investments.

What is the difference between a subsidised investment and a PPA-based renewable energy investment? A subsidised investment is based on state-guaranteed feed-in remuneration, which secures a minimum electricity price for a fixed term (typically 20 years). Regulatory risk is low, and returns are moderate and predictable. A PPA-based renewable energy investment dispenses with state subsidies and is instead based on a long-term private contract with an electricity buyer (industrial company or utility). PPAs offer greater flexibility in price setting, but require deeper market expertise and depend on the buyer’s creditworthiness. In Europe, the PPA model is on the rise, especially for new solar and wind projects without state support.

What risks are involved in renewable energy investment? The key risks are: regulatory risk, resource risk (weather dependence of generation), construction risk in greenfield projects, technology risk in newer technologies (battery storage, hydrogen), interest-rate risk in project financing and counterparty risk with PPA buyers. A well-diversified renewable energy investment across technologies, regions and contract terms significantly reduces most of these risks.

How does onshore wind differ from offshore wind as a renewable energy investment? Onshore wind offers lower investment costs, simpler financing structures and is suitable for medium-sized institutional allocations. Returns are moderate. Offshore wind offers higher capacity factors, but is significantly more capital-intensive, requires complex project finance and carries increased construction risks. As a renewable energy investment, offshore wind is primarily accessible to very large institutional investors and specialised infrastructure funds with corresponding technical know-how.

What role do battery storage systems play in renewable energy investment? Battery storage systems (BESS) are system-critical for integrating volatile renewable generation and are rapidly gaining importance as an independent renewable energy investment. Investments in BESS have tripled since 2021. Cash flows arise from capacity markets, frequency regulation and energy arbitrage. The segment requires specialised technical and market expertise, but offers attractive risk-adjusted returns and systemic importance that favours stable long-term framework conditions.

Why is renewable energy investment particularly relevant for ESG-oriented institutional investors? Renewable energy investment is one of the few asset classes that directly and verifiably combines financial return and measurable ESG impact. Investments in solar, wind or storage can be clearly classified under EU Taxonomy Article 9 or Article 8. They contribute directly to the net-zero commitments to which many institutional investors have publicly committed themselves. At the same time, renewable energy investments are well classifiable under SFDR and offer investors robust ESG reporting to their own stakeholders.

This Area on ASSETPHYSICS

ASSETPHYSICS follows global renewable energy investment with a focus on institutional real asset investors. The category covers news on fund closings and fundraising in the energy sector, deal analyses, market commentary on the energy transition, regulatory developments, context on power purchase agreements, battery storage, offshore wind and hydrogen, as well as macroeconomic contextualisation for institutional portfolio decision-makers. The specialist contributions complement the daily news feed with analytical depth and strategic context.