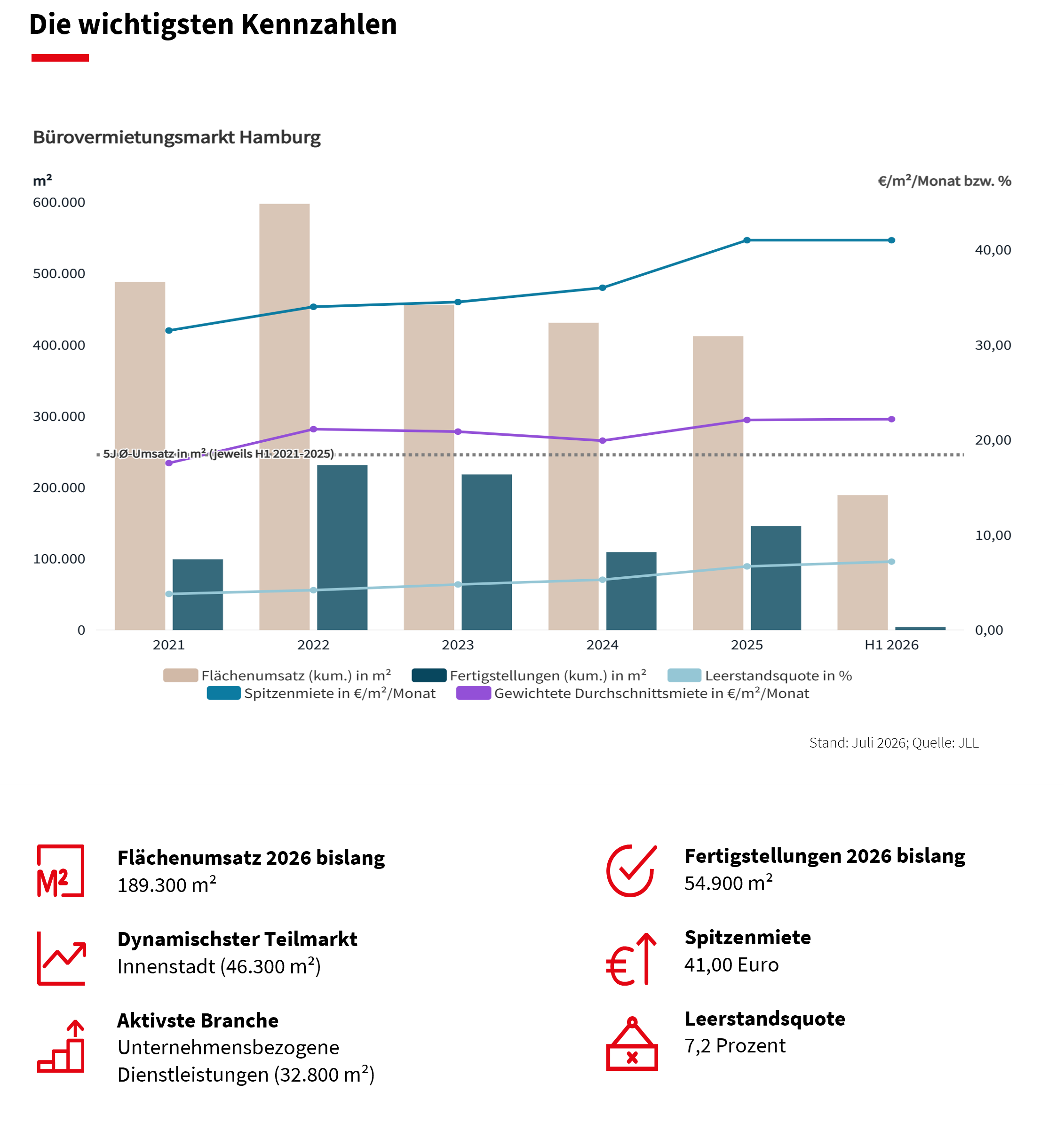

according to a new study by international real estate consultant Savills, European hotel transaction volume rose to €23.6 billion in 2025, an increase of 4.8% year-on-year. Increasingly, creative transaction models will also shape the market, Savills predicts.

According to Savills, improved liquidity, better aligned pricing expectations and robust RevPAR[1] performance across Europe (+5.4% compared to 2019, adjusted for inflation) are supporting regained investor confidence. The report highlights the growing interest in value-add strategies, with an increase in creative transaction approaches such as M&A activities and partnerships with operators expected in a market environment in the hotel real estate market that is considered to be promising overall.

Savills predicts that a number of factors will shape the industry over the next two to three years, including greater relevance of hotel operations’ operational performance, which is increasingly emerging as a key driver of returns. Against the backdrop of limited yield-interest cost spreads, the operator’s operational excellence and the ability to successfully position itself in a later market phase become significantly more important. Savills highlights that the gap between average and top-tier operators is widening, making the property’s operational performance more of a focus of investment decisions.

The research suggests that the German hotel market in particular is at a potential turning point. Although the market remains the most burdened in Western Europe after the pandemic, supply growth is now slowing significantly. The average RevPAR in 2025 was still 11 percent below the level of 2019. At the same time, rising costs are increasingly weighing on the operating results of hotels. The burden on operators is most evident in the prevailing lease models, with an increasing number of tenant insolvencies. These developments indicate a structural shift towards more creative solutions, especially with regard to the distribution of opportunities and risks between property owners and operators. This opens up opportunities for well-capitalized, long-term investors who are willing to support the market transition.

The demand of many investors is concentrated on prestige properties in prime locations, with the luxury segment in particular outperforming the overall market. The synergy effects between luxury hotels and branded residences are also increasing: the number of projects in Europe increased from 18 in 2015 to 62 in 2025 and is forecast to double again by 2032.

Large international hotel chains have grown rapidly: their average brand portfolio has almost tripled in the last ten years. At the same time, the volume of so-called key money payments — i.e. one-off financial contributions from hotel operators to owners to secure attractive locations or long-term management or franchise contracts — has increased significantly, reaching a total of $1.2 billion in 2025 for the five largest operators. With changing market conditions, Savills sees increasing potential for a shift from purely capital-poor, asset-light growth to more focused investment-right models that include more targeted equity investment. Selective investments and broader partnerships with real estate investors could help support the chains’ further expansion in the future.

David Kellett, Head of Hotel Capital Markets EMEA at Savills, says: “The European hotel investment market is entering a phase that requires conviction. Even though the operational and capital market-related environment is more complex than in previous cycles, the structural fundamentals of the travel and hospitality industry remain extremely compelling. Demand continues to prove resilient, high-quality hotel properties attract large amounts of global capital, and hotels still have the unique ability to adapt over the cycle. For investors willing to look beyond short-term fluctuations, this remains a sector full of opportunities.”

Thomas Emanuel, Head of Hospitality Thought Leadership for EMEA at Savills, adds: “Whether through recapitalisations, platform transactions, lease restructurings, co-investments or partnership-oriented strategies, the next wave of activity in the European hotel investment market will be characterised by innovation and collaboration rather than purely price factors. We are confident that the hotel sector is able to deliver sustainable, risk-adjusted returns to those who are willing to act thoughtfully and decisively.”

Tina Haller, Director Capital Markets and Head of Hotels Germany at Savills in Germany, comments: “Interest in hotel real estate has risen significantly again among investors. However, Germany, as one of the most important hotel markets in Europe, presents a differentiated picture: While occupancy, RevPAR and ADR[2] have developed very dynamically since the pandemic, many hotel businesses are coming under economic pressure due to significantly increased costs – for example for staff. We therefore expect investors to continue to be selective and increasingly rely on close partnerships with well-capitalized operators and established brands. On both the operator and the investor side, those who are willing to rethink their previous operating model and reflect more strongly on the challenges of the respective partner will benefit. “

[1] Revenue per Available Room

[2] Average Daily Rate