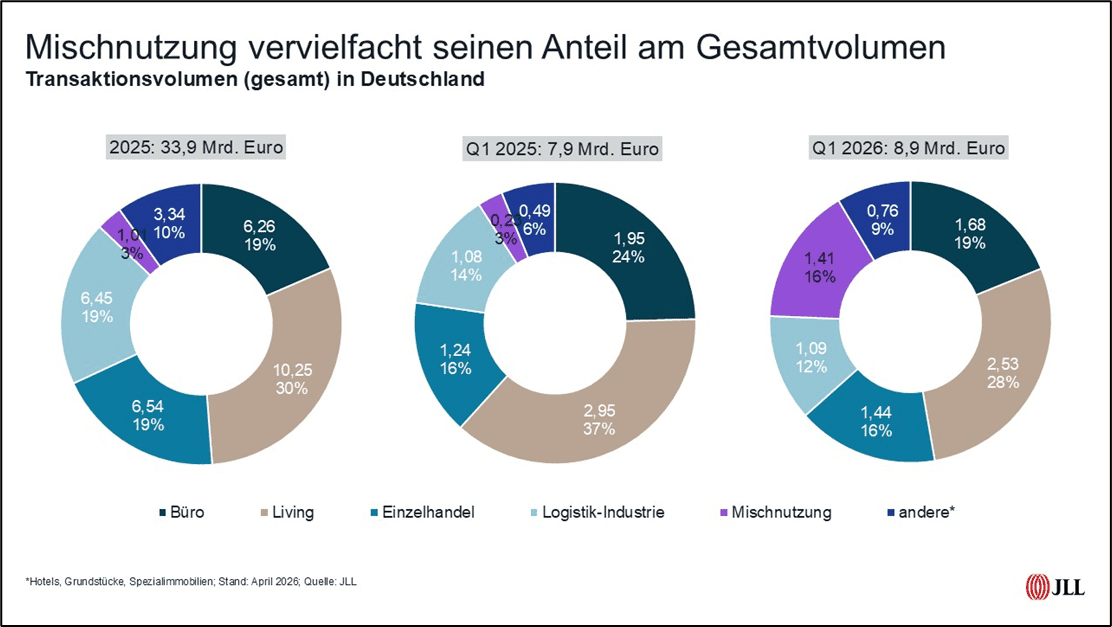

Transaction volume at the start of the year is slightly higher than last year at just under nine billion euros

Inflation is back and with it the “bogeyman” for real estate investors: rising financing interest rates. No reliable data is yet available, but everything indicates that the inflation rate in the euro area and also in Germany rose from 1.9 percent to over 2.5 percent in March. The war in Iran and the Middle East is thus gradually having an impact on the cost of living for consumers and is leaving its mark on the balance sheets, especially of energy-intensive industrial companies. This is linked to a look at the European Central Bank (ECB) and how it will behave this time, after it was said to be too hesitant during the last price increase as a result of the Ukraine war. In March, the ECB had left interest rates unchanged, and the next interest rate decision is due at the end of April. On the other hand, reactions have already been observed in the credit and bond markets: swap rates and current yields on government bonds have already risen significantly.

Despite these ongoing geopolitical risks and higher financing interest rates, the German real estate investment market is showing a moderately positive picture in the first quarter of 2026. The nationwide transaction volume reached 8.9 billion euros at the beginning of the year, twelve percent higher than the previous year’s figure.

Konstantin Kortmann, CEO JLL Germany & Head of Capital Markets: “The underlying sentiment on the German investment market for real estate developed very positively in the final quarter of 2025 and at the start of 2026. There are several reasons for this: On the one hand, only a few people speculated that interest rates would fall further, and on the other hand, the availability of borrowed capital has continued to rise.”

However, the current escalating geopolitical situation, including the energy crisis and rising interest rate expectations, has ensured that this dynamic has lost momentum, Kortmann observes. The consequences have an impact on the entire economy worldwide and their consequences are not yet clearly foreseeable.

“Deals with an interest rate well above the borrowed interest rate will continue to pay off, even if interest rates rise moderately. Then it’s more a question of price than whether the transaction is even possible. In the short term, however, we also see some market players who have been taking a wait-and-see approach in recent weeks and do not want to take any supposed risks,” adds Kortmann.

The starting position of the economy in the current crisis is significantly better than in 2022

Looking at the overall economic situation, there seem to be parallels to 2022 in the current situation. But: “A significant difference, however, is that inflation is currently around two percent, in contrast to back then, when inflation had already reached four percent before energy prices began to rise,” analyzes Helge Scheunemann, Head of Research at JLL Germany. Other differences lie in the current greater resilience of supply chains – which is one of the reasons why freight rates have only risen moderately so far – and in a generally significantly higher interest rate level. “And paradoxically, the weakening economy and weak consumption could ensure that prices increase only moderately. Based on this bundle of arguments, we expect the ECB to raise interest rates twice moderately this year. Ultimately, however, a lot will depend on hope: on the one hand, that the duration of the conflict does not last for weeks or even months after an apparent rapprochement in the past few hours and, on the other hand, that second-round effects such as higher wage agreements or the passing on of higher purchase prices do not occur or only moderately,” says Scheunemann. But these are speculations at the moment and no one can predict the development of the geopolitical situation.

This makes it all the more important to take a prudent and sober look at the facts, even if this may lead to further postponements or changes in the strategic orientation for some real estate transactions. “What we can take away and confirm for the first quarter, however, is that transaction processes that have already been initiated are continuing and that we see hardly any signs that investors with purchase intentions are completely abandoning their plans,” Kortmann notes.

Individual transactions beyond the seven metropolises give the market a positive impetus

The investment market is developing quite heterogeneously: The growth in transaction volume of twelve percent in individual transactions is particularly significant: The volume here rose by almost 24 percent to 6.7 billion euros, while portfolio transactions still lack momentum. Here, the volume fell by twelve percent to 2.2 billion euros. It is striking that the increase in individual deals did not necessarily take place in the seven largest metropolises. Here, the transaction volume almost stagnated at 3.1 billion euros and recorded only a moderate increase of just under two percent compared to the previous year. By contrast, the investment volume increased more significantly outside the seven metropolises (plus 19 percent), the share of the total volume thus rose to just under 65 percent.

Nevertheless, it is worth taking a second look at the seven strongholds. The regional dynamics show clear differences. While Berlin had to accept a decline of 43 percent to 780 million euros and the volume in Stuttgart also fell by ten percent to 90 million euros, the other five strongholds showed a consistently positive performance. In particular, Cologne with a significant increase of 122 percent and Frankfurt with a plus of 80 percent are providing growth impulses, but the volume in Frankfurt in particular remains modest at 270 million euros. There is still a lack of the office deals that are so typical of the banking metropolis.

The entire German investment activity remains characterized by small and medium-sized deal sizes; Transactions of 100 million or more continue to be the exception despite a positive development. In the first quarter, 16 transactions in excess of 100 million euros were registered, seven more than in the same period last year. By far the largest transaction to date was the acquisition of 80 percent of Cofinimmo shares by Aedifica. The pro rata value of the nursing home portfolio with 58 properties in Germany was around 750 million euros.

As in previous quarters, the “Living” asset class is once again asserting itself as the strongest category at the beginning of 2026 with unabated high demand. Overall, the share of over 2.5 billion euros is 28 percent. Office properties follow in second place with just under EUR 1.7 billion and retail and mixed-use properties with a transaction volume of around EUR 1.4 billion each. In the retail sector, the recovery continues, with food-anchored markets in particular continuing to be in demand and proving resilient. “The market situation remains challenging for office properties, and the discussion about office workplaces in the age of AI is also a factor here,” Scheunemann notes. Logistics real estate is only behind this group with a share of twelve percent. The current transaction volume of just under 1.1 billion euros – the same amount as in the previous year – corresponds to a weak start to the year. “The logistics sector, as a particularly vulnerable asset class to geopolitical and economic events, reacts very sensitively to uncertainties that can affect supply chains. At the same time, there is a lack of adequate products, especially in the core segment,” says Scheunemann.

The spectrum of buyers was relatively broad in the first quarter. Asset and fund managers traditionally form the largest investor group, accounting for 32 percent of the transaction volume in the first quarter. In addition to these buyers who invest for third parties, the public sector also plays an important role in second place (twelve percent), albeit with different investment motives depending on the asset class. In the office segment, it often acts as an owner-occupier, while in the residential segment, municipal housing companies act as buyers and thus pursue housing policy goals. The investor spectrum is supplemented by private capital (eleven percent), which continues to actively participate in market events and is dependent on less debt capital thanks to often higher equity ratios. There was little activity from open-ended mutual funds in the first quarter, as they are confronted with outflows of funds from private investors. As in the previous year, this group is likely to appear more often on the seller side than on the buyer side in the course of the year.

Yields remain at their previous year’s level – but risk premiums are eroding

The yield development on the German real estate investment market in the first quarter of 2026 shows stability across asset classes that is likely to be surprising, at least at first glance. “On closer inspection, however, the returns reflect the development described at the beginning that transactions that were already initiated in 2025 have now been brought to the finish line. Nevertheless, changes in interest rates in the further course of the year may lead to a shift in the risk-return ratio, which would be of considerable importance for investors,” Konstantin Kortmann differentiates.

The aggregated net initial yield for top office properties in the seven metropolises remained at 4.31 percent in the first quarter, at the level of the end of 2025. In the retail sector, prime yields for the sub-asset classes of commercial buildings, shopping centres and retail parks also remained stable. Prime yields in logistics and industrial real estate also remained unchanged at 4.56 percent, which is an expression of an increasing market consensus between sellers and buyers.

But while real estate yields stagnated, the bond market underwent a dramatic development: “The yield on ten-year German government bonds rose to more than 3.0 percent at times in the first quarter of 2026, the highest level since 2011.

As a result, the risk premium for an office property investment compared to German government bonds fell to only around 146 basis points, after it had been 210 basis points at the end of 2024 and 159 basis points at the end of 2025. “From a theoretical perspective, a compressed risk premium could lead to higher yields on real estate – in other words, falling prices. But some specific market mechanisms delay or prevent such an adjustment – for example, unlike the majority of government bonds, rents are indexed to inflation, which is also something that investors are beginning to take into account in times of higher inflation expectations,” says Scheunemann.

Many owners continue to “sit out” and avoid sales below book value. “This behaviour is supported by increased capital values in some areas, for example if an increase in rents could be achieved. In addition, German banks have so far only sold larger NPL portfolios in isolated cases, as the pressure to sell is not as great as in the financial crisis due to lower debt ratios. And last but not least, there is plenty of capital based on current market values, especially from international investors.” The longer the uncertainties in the Middle East persist and the USA is no longer seen as a stable anchor, capital flows could be directed to Europe and also to Germany.

“For investors, this still means cautious and prudent action, a strict examination of the sustainability of cash flows, a focus on high-quality, defensive properties with long-term leases or the acquisition of existing properties with renovation and value enhancement options,” Kortmann interprets the current macroeconomic and political situation.

Giving a forecast for 2026 as a whole is currently like looking into a crystal ball, and the impact of the geopolitical upheavals cannot yet be measured, especially the medium-term consequences for further interest rate developments. “Based on the current status and with a view to the properties and processes on the market, we expect a total annual result of 35 billion to 40 billion euros,” Helge Scheunemann looks ahead.