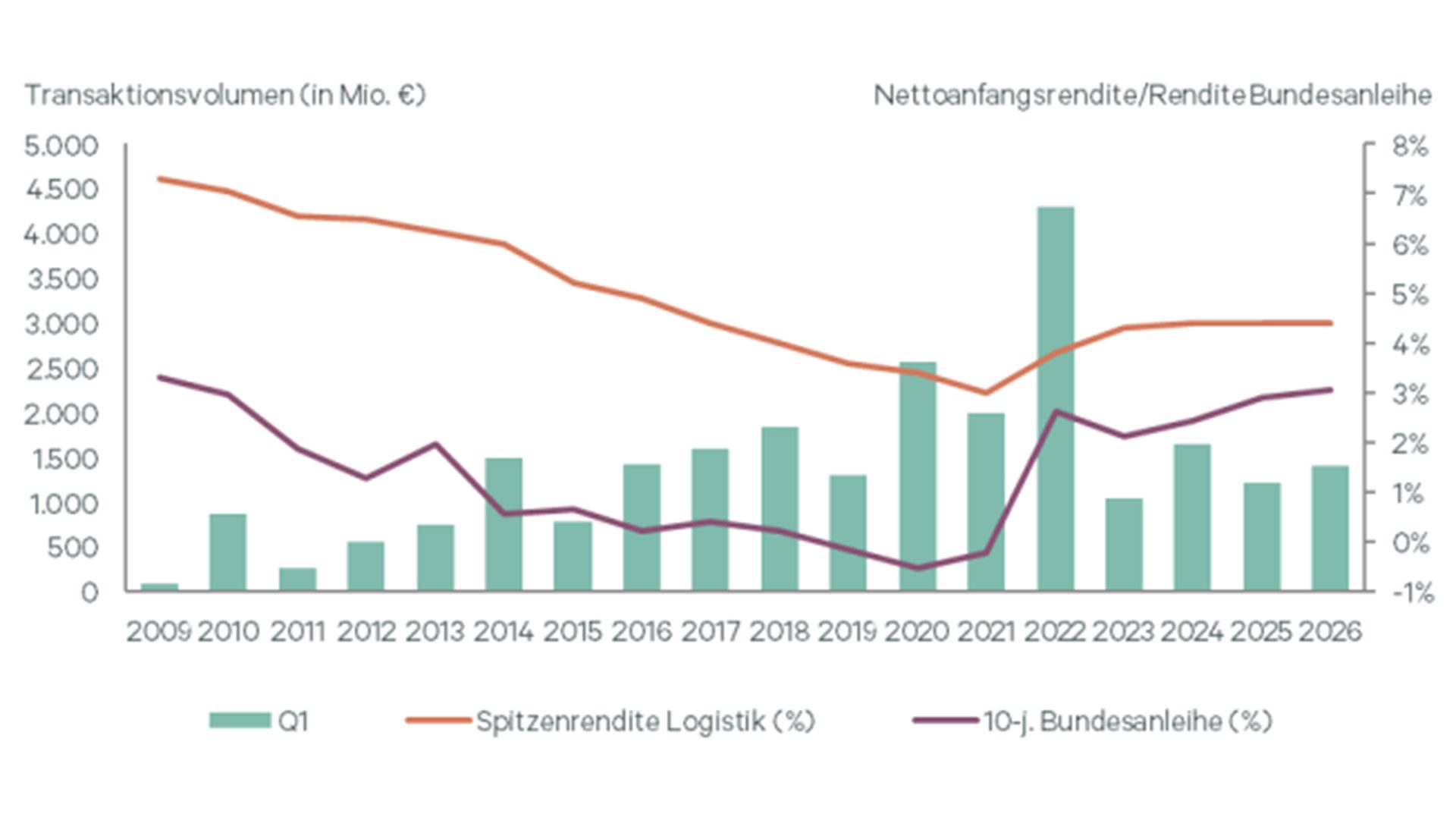

The German industrial and logistics real estate investment market reached a transaction volume of EUR 1.4 billion in the first quarter of 2026. This exceeded the volume of the prior-year quarter by 16 percent. The share of logistics properties decreased slightly (minus 13 percentage points to 70 percent), while Light Industrial increased by twelve percentage points to 18 percent. Production real estate remained almost stable at eleven percent. The importance of the top 7 cities in terms of transaction volume declined noticeably – by ten percentage points to just six percent. Portfolio transactions gained slightly in importance, with a share of 21 percent (up nine percentage points). These are the results of a recent analysis by global real estate services provider CBRE

“A dynamic start to the year became more cautious from March onwards due to the geopolitical situation. Nevertheless, the previous year’s result was noticeably exceeded. Interest remains high – there are numerous sources of capital, especially from abroad, who want to establish and expand their logistics presence in Germany,” says Kai F. Oulds, Head of Industrial & Logistics at CBRE in Germany. At 71 percent (up one percentage point), the share of international investors remained at the high level of the first quarter of 2025.

“Interest is being boosted by positive impetus from the user market in terms of vacancies and attractive leases,” adds Kristine Kühn, Senior Director Valuation Advisory Services at CBRE.

Compared to the first quarter of 2025, Core and Core Plus properties each increased their share of the transaction volume slightly (Core by plus eight percentage points to 34 percent and Core Plus by plus two percentage points to 26 percent). Investments in value-add real estate, on the other hand, had to record a decline of twelve percentage points to 20 percent. Opportunistic investments accounted for a share of 16 percent (up five percentage points). Owner-occupiers played practically no role at the start of 2026. “The decline in transaction volume in the value-add segment is mainly due to a lack of product offering,” says Tom Franke, Head of Logistics Investments at CBRE. This is because international investors in particular continue to show great interest here.

We have recently seen fewer sale-and-lease-back transactions. This is because potential sellers often have inflated price expectations that do not yet correspond to the current market level,” says Franke. The share of corporates among sellers fell by seven percentage points to 15 percent compared to the first quarter of 2025.

Outlook for the rest of 2026 “The sales pipeline is well filled. The willingness to make major deals with more than 100 million euros has also increased – but then the product has to fit exactly. In this size class, more deals are expected in 2026 than in the previous year,” explains Franke.