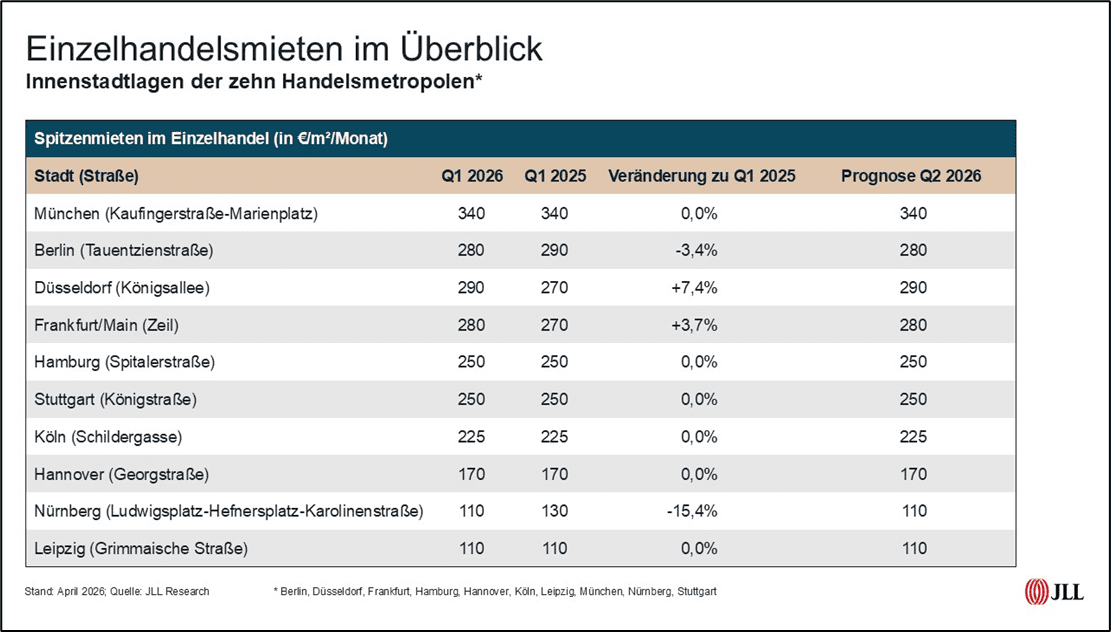

Prime rents in retail: Düsseldorf outstrips Berlin

After years in which the ranking of the most expensive shopping cities seemed to be cemented, there is now movement in the top group. Munich remains the most expensive retail location in Germany at an unchanged 340 euros/m²/month. But behind them, Düsseldorf recorded an increase from 270 euros to 290 euros (plus 7.4 percent), while Berlin had to accept a slight decline from 290 euros to 280 euros (minus 3.4 percent) and thus lost second place to Düsseldorf. The capital is now on a par with Frankfurt am Main, which climbed by ten euros to 280 euros.

Hamburg and Stuttgart remained stable at 250 euros each, as did Cologne at 225 euros, Hanover at 170 euros and Leipzig at 110 euros. Nuremberg recorded the sharpest decline with a minus of 15.4 percent to 110 euros.

Aniko Korsos, Head of Retail Leasing JLL Germany: “Prime rents are an important indicator of retailers’ confidence in Germany’s top locations. Düsseldorf has invested a lot in its city centre in recent years and now attracts an international audience in the high-price segment without being an international metropolis itself. Meanwhile, Berlin is experiencing consolidation for the first time after decades as a trend city. For the time being, there are signs of stabilization for all cities. All ten stores are expected to maintain their current prime rents.”

For the other 56 cities examined by JLL, prime rents remained unchanged in the population classes of 500,000 inhabitants and above as well as in the adjacent class of 250,000 to 500,000 inhabitants. In the smaller cities with 100,000 to 250,000 inhabitants and less than 100,000 inhabitants, prime rents were also stable. In the Germany-wide average of all 66 cities examined, the rent level thus remained almost constant.

For the other 56 cities examined by JLL, prime rents remained unchanged in the population classes of 500,000 inhabitants and above as well as in the adjacent class of 250,000 to 500,000 inhabitants. In the smaller cities with 100,000 to 250,000 inhabitants and less than 100,000 inhabitants, prime rents were also stable. In the Germany-wide average of all 66 cities examined, the rent level thus remained almost constant.

Take-up returns to the 100,000 m² mark

Meanwhile, after last year’s soaring performance, the market has made a somewhat more modest start to 2026: 103,100 m² of retail space was rented in the first quarter. This take-up is almost ten per cent below the current five-year average of 115,200 m² for a first quarter. A total of 171 deals were counted. Although this is at the level of the previous quarter with 174, this had already meant a setback from 232 deals.

“The shift in the structure of leases is remarkable: the share of deals in the ten metropolises rose to 49 percent in the first quarter of 2026 – the highest figure since the third quarter of 2023. This indicates that strategic leases are still being implemented despite the overall subdued demand. At the same time, the share of international concepts also reached a peak of 56 percent, which underlines the attractiveness of the German retail market for global players,” says Aniko Korsos.

“The shift in the structure of leases is remarkable: the share of deals in the ten metropolises rose to 49 percent in the first quarter of 2026 – the highest figure since the third quarter of 2023. This indicates that strategic leases are still being implemented despite the overall subdued demand. At the same time, the share of international concepts also reached a peak of 56 percent, which underlines the attractiveness of the German retail market for global players,” says Aniko Korsos.

Among the ten most important retail markets, Berlin achieved by far the highest letting take-up in the first quarter of 2026 at 23,700 m². This corresponds to a significant increase of 91 percent compared to the same quarter of the previous year and underlines the outstanding position of the capital as an expansion destination in the German retail sector.

The NRW state capital Düsseldorf follows in second place with 7,500 m² and also recorded strong growth of 47 percent compared to the previous year. Hanover completes the top trio with a total of 4,700 m² and an increase of 62 percent – a remarkable result for a traditionally smaller market.

The classic retail strongholds, on the other hand, are much more subdued: Stuttgart achieved a minus of 25 percent with 4,100 m², while Munich lost around 41 percent with 3,800 m². The significant declines in Hamburg (minus 70 per cent to 3,200 m²) and Frankfurt/Main (minus 78 per cent to 1,900 m²) are particularly striking.

Jack & Jones, Primark and Lefties are on course for expansion

In a sector comparison, the textile trade accounted for a total of 28 percent of the area – still the top spot among all sectors. With around 28,700 m² of leased space, the sector is proving to be the most important driver of the retail letting market in the first quarter of 2026. The Jack & Jones brand was particularly active with three new leases. Primark and Lefties also contributed to the expansion dynamic.

The second strongest sector was once again the gastronomy/food sector, which rented 21 per cent of the total volume or around 21,700 m². The majority of the deals come from the gastronomic segment. Among the most expansive formats in the first quarter were Edeka, Goldies and 60 seconds to napoli, each with several new leases.

")