Tobias Moroni ist Managing Director Fund Platform in der Institutional Investment Group. Davor war Tobias Moroni bei Hauck & Aufhäuser, zuletzt als Mitglied des erweiterten Vorstands (Executive Board) für das Kerngeschäftsfeld Asset Servicing in Deutschland & Luxemburg und zuvor Leiter der rechtlichen Einheit der Depotbank von Sal. Oppenheim.

Institutional Investment Partners (2IP) bündelt innerhalb der Institutional Investment Group (2IG) relevante Leistungen für institutionelle Anleger mit dem ausschließlichen Zweck, gerade im Zusammenspiel mit den Immobilien- und Infrastruktur-Managern den maximalen Mehrwert im Mandat auszuschöpfen.

MIPIM can now also be followed remotely – via LinkedIn, photos and weather reports from Cannes. While the industry is discussing the sun and umbrellas, a new real asset class is growing in the background: buildings for algorithms.

The exit for special real estate funds: If real estate markets do not fit the fund calendar, the planned exit strategy quickly turns into a sober weighing up between liquidation, extension – and the consequences.

It is becoming increasingly apparent that real estate funds are perceived as particularly viable institutionally in two forms in particular: as very large open-ended vehicles or as closed club structures.

AI makes office properties less plannable and CapEx has to be rethought.

The current discussion about modern office real estate is often conducted as a CapEx question. This view now falls short.

Rising defense spending is driving demand for industrial and logistics real estate. But not every defense space is a fund product – location, exit and investor acceptance are decisive.

Fund contracts are becoming more and more complex. At the same time, central questions of risk and responsibility are shifting: side letters have become the place where institutional investors try to anchor responsibility where it can no longer be clearly regulated in the contract.

In an interview with Dr. Andreas Peppel, Tobias Moroni classifies charging infrastructure from an investor's point of view – between structural tailwind and operational complexity.

Infrastructure remains in place – but in 2026, speed, depth and filters will once again become significantly more important in the investment decisions of institutional investors.

Core stands for stability and predictability in real estate investment. But if existing properties require high reinvestments, the question arises as to whether core classifications fully reflect the real estate life cycle – and what consequences this has for exit strategies of open-ended funds.

The Dutch law on the future of old-age provision changes the allocation logic of entire pension systems. This will lead to a fundamental change in Europe's largest funded pension system.

Behind the mood in the institutional fund business, described as market uncertainty, there is actually something else: the tidying up of temporary solutions.

The document is extremely extensive, but the core message is clear: Europe should finally get a genuine, uniform capital market – and for this purpose, the supervisory and market infrastructure model will be radically standardised.

For institutional investors, the weights within real assets are shifting. Real estate remains a central portfolio element, with infrastructure increasingly supplementing it with a stability component.

Europe is finally daring to ask what a sustainable product actually is. The SFDR reform is nothing less than an attempt to bring order to a decade of regulatory chaos.

While the German AnlV diverts capital flows, Solvency II tries to accompany them in a risk-appropriate manner. Reduced capital requirements are intended to open up capital in particular for infrastructure – keyword: qualified infrastructure.

In 23 weeks, amazing projects can be realized in the real assets world – if only it didn't take so disproportionately long to raise the necessary funds. Is the fund industry an anachronistic obstructionist?

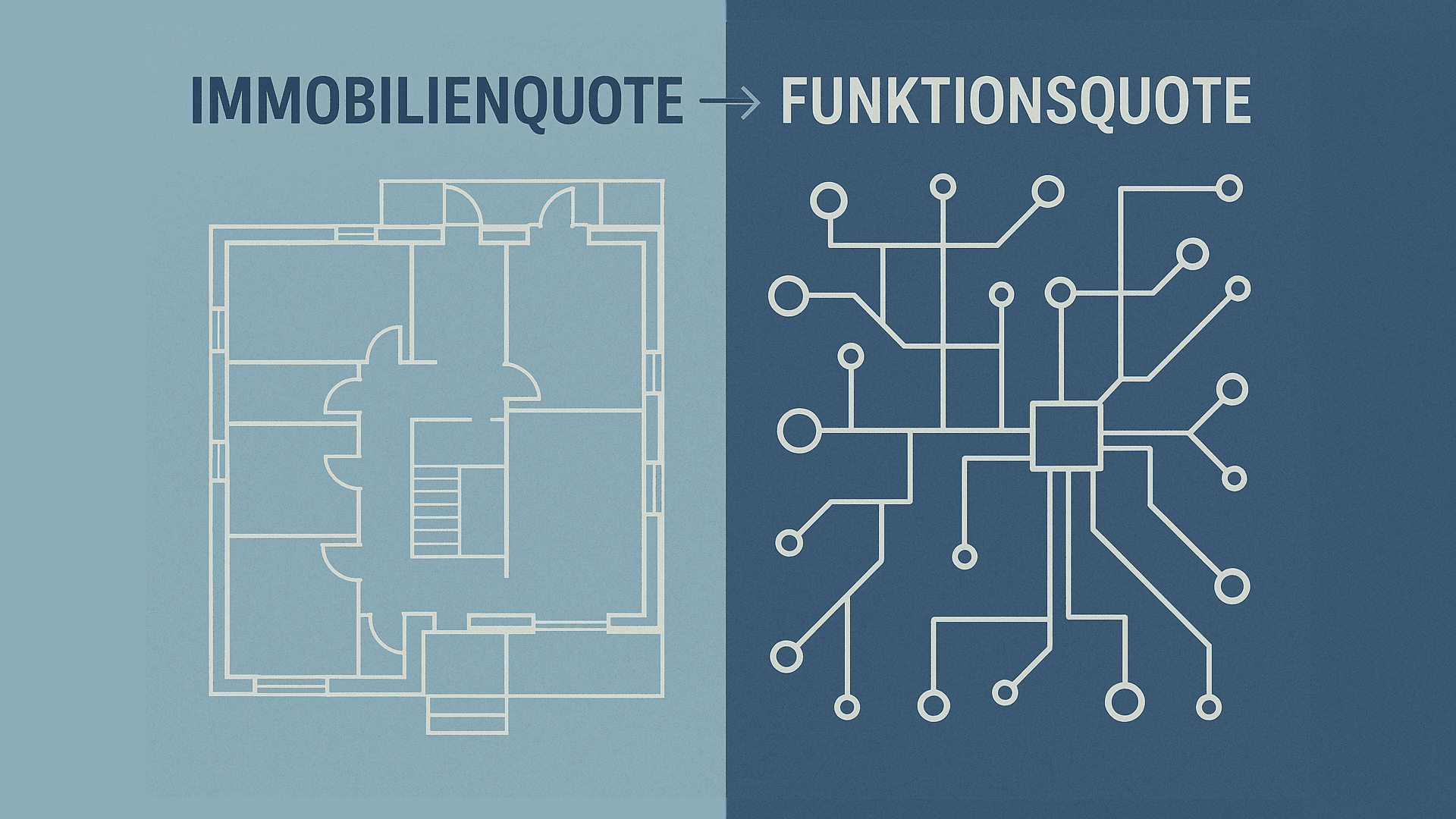

Anyone who still asks for a real estate quota in the context of institutional real asset investments today may miss the development towards a supply and function quota.

At first glance, ESMA's new Regulatory Technical Standards seem technical, detailed and difficult to digest. But if you take a closer look, you will see that these rules are not a stumbling block, but an architecture of enablement.

Institutional investors are pushing for strong responsibility governance in real estate master fund mandates. The asset manager's legal responsibility should no longer be limited to merely advising KVG's portfolio management.

In the infrastructure sector, niche business models promise returns on innovation. Naturally, this is offset by increased risks. Tobias Moroni spoke with Dr. Andreas Peppel, Managing Director at Institutional Investment Consulting Partners, about whether and how such models can be useful.

Value adjustments, refinancing pressure and changing user needs are currently encountering an oversupply of space that is no longer up to date. Tobias Moroni spoke to Dr. Oliver Voß, Managing Director at Institutional Investment Consulting Partners, about opportunities, timing and the role of net operating income.

The office sector is not currently very popular with institutional investors. Whether office properties are a discontinued model – or whether opportunities are emerging for investors from the market shakeout right now.

Open-ended real estate funds have been encountering legal grey areas in the integration of renewable energies for years. With the new Location Promotion Act (StoFöG), the legislator wants to eliminate these uncertainties.

In future, investment management companies (KVG) that set up or manage funds on the initiative of third parties will have to explain to BaFin in detail how they identify, prevent, manage and disclose conflicts of interest.

The aim is to overcome the fragmented internal market for occupational pensions and to channel the capital of pension institutions more towards long-term investments such as private equity, infrastructure, private debt and real estate.

With a whole toolbox of liquidity management tools (LMTs), the regulation aims to create more stability for open-ended investment funds in the future. But are they really a protective shield in the crisis – or in the end just a promise of good weather?

The sales apparatus in Europe has enthusiastically pounced on the ELTIF 2.0. This makes it all the more interesting to look over the fence: With the LTAF, London is showing that retail investors can organise access to illiquid investments in a completely different way.

While the fund industry is taking significant improvements in product law as a cause for celebration, regulation for asset management companies (KVGs) continues to tighten – and is moving them ever deeper into the orbit of the banking world.

Electronic fund units have been a topic in the fund industry for some time, although interest in them is only just beginning to awaken. Many isolated pilot projects in the area of so-called crypto fund shares can currently be observed.

Following the EIOPA drafts published on 10 July 2025, the EU Commission has now also submitted its proposals for amended Level II implementing provisions to the Solvency II Directive for consultation on 17 July 2025.

In its new FAQ of 14 July on the collective ruling of 19.3.2025, BaFin has clarified how insurance companies subject to the Investment Ordinance (AnlV) can allocate infrastructure investments to the new infrastructure quota as part of their reporting.

After the publication of the column "Tenant electricity from photovoltaics: possibilities and models from the point of view of the property owner", the author received a lot of feedback – especially from institutional investors.

With the "Call for Evidence for an Impact Assessment", the European Commission has called for participation in constructive criticism of the SFDR. Under scrutiny: Articles 8 and 9, the disclosure requirements and the famous principal adverse impacts.

"The knot has burst," states the introduction to the broad-based study on the ELTIF market by the analysis firm Scope. In fact, ELTIFs have become the trendsetter of recent years.

The draft of the BaFin leaflet on the influence of investors on investments and divestments of investment funds provides an opportunity to sharpen understanding of the traditional role-playing game with a long history of investors and capital management companies.

Started with enthusiasm and now at a dead end? ESG is still the right thing to do – whereby it depends on the value-creating implementation and goal with the fund strategy.