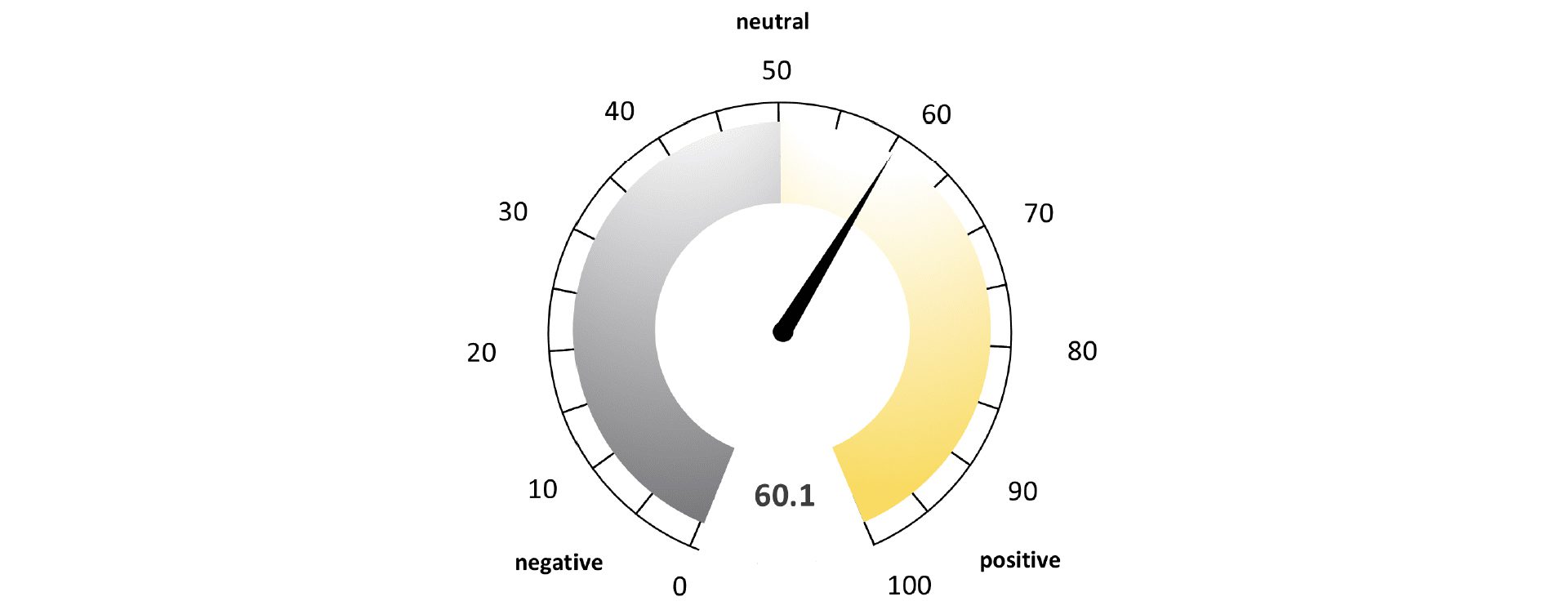

With the first issue of BF. Private Debt Market Compass, BF.capital GmbH presents a new, data-based market analysis for the international private debt sector. The panel survey collects the assessments of around 200 fund managers in the private debt sector every six months. It covers the sub-segments Corporate Direct Lending, Real Estate Debt and Infrastructure Debt. The kick-off study is based on a survey conducted in December 2025 with 67 participants from all over the world, with a focus on Europe. It shows an overall positive market environment, characterised by stable credit structures, selective competition and a robust investor base despite macroeconomic uncertainties. The first BF. Private Debt Market Sentiment Index reaches 60.1 points, well above the neutral level of 50. In particular, the robust fundraising momentum, rising capital commitments from institutional investors and balanced risk-return ratios are contributing to this positive underlying trend. The so-called expectation gap, the difference between the future and past components in the survey, also signals increasing optimism for the first half of 2026.

Stable market conditions with a slight advantage for borrowers

According to the panel, financing conditions in the private debt market have proven to be stable for the most part over the past six months, with slightly borrower-friendly tendencies. Over the next six months, the market balance will shift slightly in favor of lenders. At the level of the corporate, real estate and infrastructure lending sub-segments, leverage levels remain at the lower end of the usual market ranges. For example, the debt ratio in corporate direct lending is mostly below five times EBITDA, while the loan-to-value ratios in real estate debt are completely in the corridor of 56 to 65 percent.

Fundraising momentum is noticeably gaining strength

The positive assessment is particularly clear in the area of capital raising: More than two-thirds of the participants report increasing momentum in fundraising, and 82 percent expect further improvements in the following six months. At the same time, capital commitments from institutional investors are increasing: almost two-thirds of those surveyed are recording higher LP commitments, and no participant expects declining commitments from limited partners. Existing investors continue to play a central role in capital commitments: In some segments, the proportion of so-called re-ups – i.e. increases in existing investments – is over 80 percent.

Operational risks dominate – credit quality remains robust

According to the respondents, any stress factors in the portfolios are not primarily structurally driven by excessive debt or refinancing problems, but rather of an operational nature and sector-specific. For example, the consumer and retail-related areas of corporate financing are under particular pressure, the office and high-street retail types of use in real estate financing, and the energy sector in infrastructure financing.The ratios for non-performing or non-performing loans remained largely stable in the past six months. Almost 85 percent of those surveyed report unchanged values. The outlook for the next six months also shows only a slight tightening in individual market segments.

The full study can be downloaded from www.bf.capital .