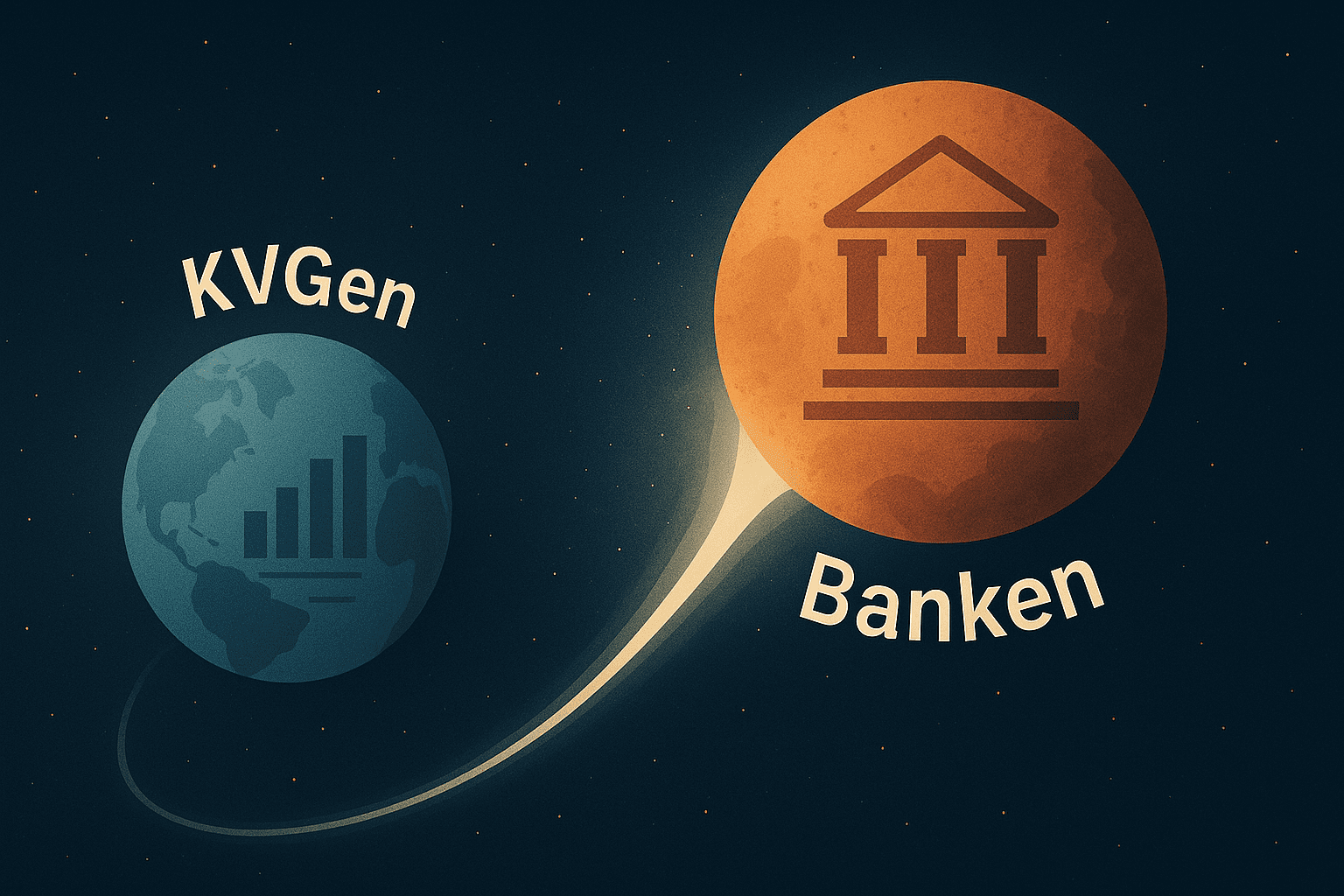

While the fund industry is taking significant improvements in product law as a cause for celebration, regulation for asset management companies (KVGs) continues to tighten – and is moving them ever deeper into the orbit of the banking world.

Government draft of the Fund Risk Limitation Act (Reg-E)

At the beginning of August, the Ref-E of the Federal Ministry of Finance was published. The consultation will last until 5 September. The background is as follows:

- On the one hand, the Reg-E does the job of the Fund Market Strengthening Act, which did not come into force in the previous legislative period in the traffic light turmoil.

- On the one hand, this includes the now urgent transposition of EU directives into national law, for example for the revision of AIMFD and UCITS.

- In addition, the Reg-E takes up other contents of the Fund Market Strengthening Act, which, according to their name, are intended to contribute to the strengthening of the German fund market, whereby some of these contents have even been significantly further developed.

Obvious (product) level

The first public reactions in the fund industry: A short media image that restricts itself to the improvements in product law. This is completely understandable, because product regulations are directly linked to the possible implementation of strategies and catch or determine the public discourse, which is reinforced by the fact that consultants working mainly in product law are involved in its formation.

And rightly so, the welcome improvements to the numerous product regulations have been very well received in the first reactions. However, the author does not want to go into this obvious (product) level in this column. Especially since advisor addresses already versed in investment law provide very good information about this in publicly accessible newsletters. There are more than enough sources of information on this.

(KVG-) Background Layer

Aside from the obvious (product) level, this column edition aims to shed light on the regulations at KVG level that entail relevant changes for the administration by the KVGs.

What is it about: It has been observed for some time that KVGs are moving closer to the regulatory system of credit institutions. A look exclusively at the Reg-E would be incomplete to describe this process. And yet the Reg-E takes up this overarching and ongoing process very clearly and colors itself through it. The shift in orientation associated with the change of name from “Strengthening Act” from the past legislative period to “Risk Limitation” should not be misunderstood.

The Reg-E therefore rightly relaxes product law, which has been positively received in the (consultant) industry. And now let’s take a look at the regulation of investment management companies themselves: The Reg-E drives the professionalisation process of the AIFMs further by imposing requirements with regard to the behavioural and organisational obligations of the AIFMs that are even closer to those of credit institutions.

It follows that the law fortunately moves away from the German tradition of achieving risk limitation through overloaded product law, but organises this beyond product law through significant tightening at the level of the KVG company. Or in short: Capital management companies are allowed to do more and more at the product level (example: debt funds), but conversely, they also have to be able to do more and more!

Examples of far-reaching requirements for the KVG that the Reg-E tightens or introduces for the first time are:

- Managing Director of KVG: Must be employed full-time by the KVG; this is particularly smaller and medium-sized providers, some of whom have involved part-time managing directors, for example if they have a high degree of expertise and are to support the expansion of the business initially; however, the provision may also have a severe impact on KVGs from corporate structures: it opens the door for specification by the supervisory authority, which is not yet foreseeable. After all, according to what standard should cases be assessed in which a group KVG organises itself in a division of labour and, for example, receives services from other group entities and the managing director of the group KVG also works for these other group entities? The judiciary tells you that full-time employment for the group KVG still exists here, because it should not matter in which company the managing director performs the work required for the KVG. Would this still apply if the group entity provides services not only for the group AIFMs, but also for third AIFMs? The entire industry is geared towards scaling and platform effects, and opening up one’s own workbench to third parties is of relevant importance for this. It can then actually make no difference whether the managing director also manages these services from the KVG for third parties or from a group entity.

- Greater transparency and integration into processes of outsourcing and sub-outsourcing companies: In the case of AIF-KVGs, the application for authorisation under currently valid section 22 (1) no. 8 KAGB only requires that “information on outsourcing agreements pursuant to section 36 KAGB” be provided; the provision that will replace it in the future requires much more documented transparency on the part of the KVG about remaining tasks in outsourcing controlling and, above all, it now applies not only to “outsourcing” but also to “sub-outsourcing”; Further responsibilities also result directly from the amendments to section 36 KAGB.

- Credit back-office: The Reg-E builds on the existing legal situation, but further tightens it: AIF AIFMs that grant loans must further expand their risk management; in addition, liquidity risk management systems must be integrated in the case of loans granted funds as open-ended investment funds.

- Reporting obligations: The reporting obligations will be extended and come a further step closer to those of credit institutions; it is also even more about capturing systemic and other market risks.

- Special envoy: Based on the provisions of the KWG for institutions, according to which a special representative can be entrusted by the supervisory authority with the performance of tasks in the capital management company.

System Convergence

The structural adjustments for asset management companies above illustrate the trend that is classified here in this column as system convergence . There is a levelling of the regulatory level of all regulated participants in the financial industry, whereby the regulation of all is based on the regulatory level of credit institutions. The Reg-E alone does not justify this trend, but is to be seen as another essential part of this ongoing process. Asset management companies are currently exposed to strong regulatory pressure from several sides, for example from the Fund Risk Limitation Act and other regulatory systems such as DORA as well as the regulation on artificial intelligence.

What follows from this and what could follow from this – results:

- Capital management companies are increasingly allowed to act more freely on the product side (more “competitiveness” compared to foreign fund locations) and in return must be able to do more and more as an organization.

- There is no stop to this professionalization trend, because credit institutions are also exposed to permanent increasing regulatory pressure, and capital management companies are moving into their orbit.

- In the future, business models will have to be thought of even more strategically through processes and business organizations, i.e. already (fund strategy and sales have long since ceased to be sufficient success factors).

- This regulatory pressure is coming up against an industry that is struggling with shrinking capital pots in the field of real estate funds; as a result, it can be assumed that synergies will be sought even more strongly between AIF capital management companies, which could ultimately lead to a reduction in the number of licensed AIF capital management companies.

- Market entry barriers for start-ups continue to rise; for private start-ups in any case, but also in the institutional sector, if you want to enter the fund business, the decision will probably be in favor of “buy” in the context of “make or buy” decisions.