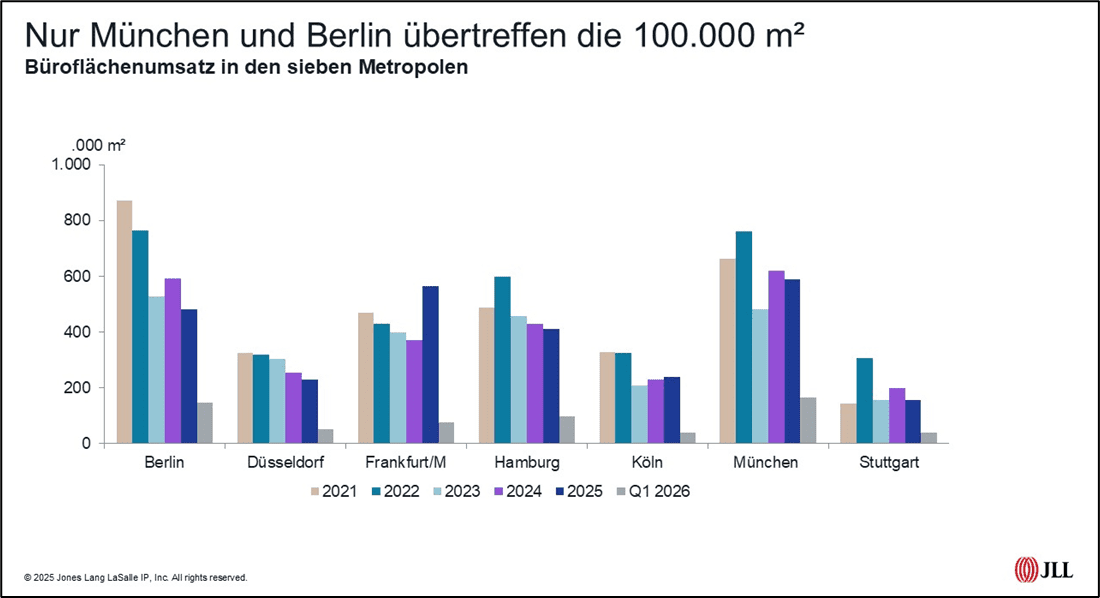

At 617,000 m², take-up in the seven metropolises is significantly below the previous year’s level

Sentiment among companies in Germany deteriorated noticeably at the end of the first quarter. The ifo Business Climate Index fell to 86.4 points in March, after 88.4 points in February. This was mainly due to significantly more pessimistic expectations, but the assessment of the current situation remained unchanged. The results reflect exactly what can be observed in the real estate markets: 2026 had started with a lot of confidence, the economy is showing the first signs of recovery and as a result, companies have also gained confidence. And now? Uncertainties are increasing again and the consequences of the war in Iran, which are not yet fully foreseeable, are putting an end to hopes for a sustainable upswing for the time being. This is also reflected in the German office letting markets: with cumulative take-up of 616,800 m² in the seven largest metropolises (Berlin, Düsseldorf, Frankfurt, Hamburg, Cologne, Munich, Stuttgart), 2026 got off to a subdued start and is around 17 per cent below the figure for the same quarter of the previous year.

Konstantin Kortmann, CEO JLL Germany: “It affects all sectors equally, from energy-intensive industry and construction to trade and services. What unites the prospects is the fear of a return of inflation, which could then have another impact on the German economy in the further course of the year via second-round effects. Cost efficiency is and remains a central issue from the company’s point of view. At the same time, space optimisation is also moving further up the agenda of companies.” At the same time, Kortmann sees a shortage of modern and high-quality space: “At the same time, however, project developers are also affected by rising construction costs, which could reduce the supply of new office properties for this year and next year, so that users will be confronted with less choice and higher rents for premium space in sought-after locations.”

From a real estate perspective, companies have come to terms with the “new normal” and accepted the relative unpredictability. The world and the environment are different than they used to be and will remain different, yet decisions are made and deals are made in such an environment. Nevertheless, JLL does not expect any dynamics resulting from company expansions. “The new enquiries and applications serve as an indicator for the further course of the market, here it was very quiet in the first quarter. However, there are still many ongoing enquiries and large-volume enquiries also support our outlook for the year as a whole, as does the observation that hardly any enquiries have been withdrawn so far,” says Miguel Rodriguez Thielen, Head of Office Leasing JLL Germany. “We are therefore revising our annual forecast only slightly downwards and now expect moderate growth in the single-digit percentage range compared to 2025.”

Munich and Berlin together account for half of the take-up of space in the seven metropolises

“Overall, economic trends and continued reluctance to make leasing decisions, rising vacancies and increasing polarisation are shaping the markets. At the same time, the rent level in the top range is stable, driven by unbroken demand for high-quality, modern and sustainable space in central locations,” analyses Helge Scheunemann, Head of Research at JLL Germany.

However, the market development is heterogeneous. While the megacities of Munich and Berlin recorded a robust start to the year, other markets were more cautious. Munich with 164,900 m² and Berlin with 148,100 m² together account for more than half of the total take-up. In Munich in particular, where take-up was 17 percent higher than in the same quarter of the previous year, several major deals made a significant contribution to the strong result. These include leases from JetBrains (21,500 m²) and E.ON (21,300 m²), which underline the continued strength of the industrial and IT sectors. In Berlin, too, there was a slight upturn in demand in all size classes and sectors.

“In other markets such as Düsseldorf (51,200 m²), Cologne (40,400 m²) and Stuttgart (38,200 m²), however, we observed delayed decisions and an overall lower number of new major deals. In Düsseldorf and Cologne, for example, only one deal with more than 5,000 m² was registered. However, there are still some current applications of this magnitude in these cities,” says Rodriguez Thielen.

In general, many companies are currently examining an extension of their existing leases as the first option. For owners, this means that active asset management also creates opportunities to retain their existing tenants if they offer attractive conditions.

Structural shortage of modern space intensifies, renovation rate rises significantly

In addition to the change in the occupied office space stock – in the past twelve months, this figure fell by around 139,000 m² across all seven strongholds – the total vacancy rate in these markets continued to rise significantly, reaching a volume of 8.3 million m² in the first quarter of 2026. The vacancy rate climbed accordingly to 8.3 percent, compared to 8.1 percent at the end of 2025. The highest rates are in Düsseldorf with 11.6 percent and Frankfurt with 10.4 percent. The lowest rate continues to be recorded in Cologne with 5.1 percent.

“However, the increase in vacancies must be viewed in a differentiated way. The gap between modern, well-equipped properties in central locations and properties in B and C locations in need of renovation is widening. Tenants are specifically asking for space that offers high quality, good infrastructure connections and a high quality of stay, while older portfolios are increasingly coming under marketing pressure. This scissor trend is not new, but it is currently becoming more and more entrenched, even though rents continue to rise at the peak,” explains Helge Scheunemann.

The market for sublet space, which has grown strongly in recent years, continues to stabilize and in some cases space is even taken off the market again because the companies use it themselves. Across all seven locations, the volume of space offered for subletting amounts to 833,700 m², which corresponds to 0.8 percent of the total stock.

The regional discrepancy is also manifested when looking at the volume of completion. In the first quarter of 2026, a total of 275,100 m² was completed in the seven largest German office markets. Of this volume, 85,800 m² was accounted for by Berlin alone, followed by Frankfurt with 66,700 m² and Hamburg with 50,700 m².

“However, of the space completed in the seven metropolises, only 95,000 m² (35 per cent) was still freely available on the cut-off date, while the rest were already occupied by tenants and owner-occupiers. This underlines the continuing high demand for modern, sustainable new construction projects, especially in prime locations,” Scheunemann differentiates.

According to the current status, 811,600 m² are under construction for 2026, of which 38 percent are already occupied. A significantly higher completion volume is expected for 2027: a total of 1.43 million m² is in the planning stage or already under development, with Berlin with 575,600 m², Munich with 387,000 m² and Frankfurt with 156,900 m² having the largest volumes.

“In view of the expected price increases, including for building materials such as cement, the situation in the construction industry threatens to deteriorate again. It therefore seems realistic that there will be time shifts, so that at least the 2026 and probably also the 2027 new construction volume is unlikely to lead to a significant reduction in the supply shortage. The structural shortage of modern office space will continue in the medium term,” Scheunemann expects.

At the same time, this can be an opportunity to invest in existing buildings, especially if office stock can no longer be used sustainably. And the figures prove that owners are reacting: Of the total volume of new construction in 2026 and 2027, 38 and even 40 percent respectively will be accounted for by renovations – a significant increase compared to previous years, when renovations accounted for only eight to 17 percent of new buildings. In addition, JLL expects that the topic of conversions will also come back into focus, not least due to the recently approved federal funding of 300 million euros. Vacant offices could thus become alternative uses such as housing, hospitality, coliving, education, fitness, medical and social facilities.

Prime rents remain stable despite higher vacancy rates

Despite the growing supply, prime rents in prime locations remain stable or grow slightly. The “flight-to-quality” trend means that the demand for premium space exceeds the scarce supply in this segment. “Companies continue to pay a premium for modern, sustainable and well-located space. These criteria are crucial for recruitment, increasing office occupancy rates, and meeting ESG criteria. In the data analysis, these trends are particularly evident when looking at the rents of completed lettings of very high-quality space, which continue to rise, and on the other hand, falling rents for office space with low furnishing standards,” says Miguel Rodriguez Thielen, describing the spread in the market.

Munich leads the rent ranking with a prime rent of 60.00 euros/m², and within the past twelve months the rent has risen by 7.1 percent. Hamburg achieved even stronger growth. In the meantime, 42 euros/m² are paid at the peak in the Hanseatic city, an increase of almost 17 percent year-on-year. On average across all seven strongholds, rents rose by 5.3 percent over the past twelve months. By the end of the year, JLL expects further slight prime rent increases in almost all strongholds, so that the JLL prime rent index is then likely to be 2.5 percent above the year-end value of 2025 at 313.3 points.