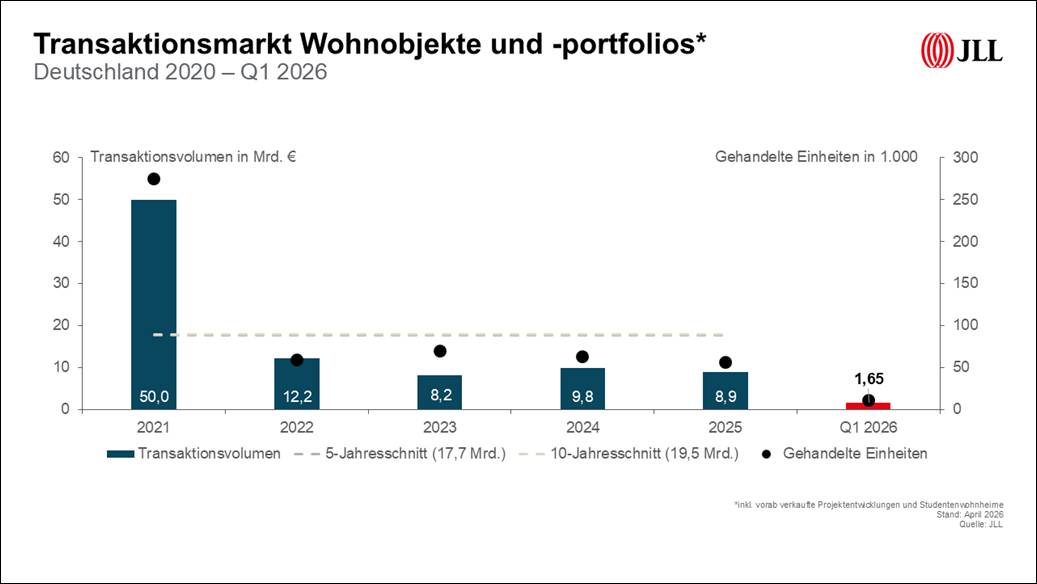

Selective investor behaviour and smaller deal sizes characterise the German residential investment market in the first quarter of 2026. At EUR 1.65 billion, the transaction volume is significantly below the previous year’s figure (EUR 2.35 billion). However, market activity remains at a solid level with 57 registered transactions (Q1/2025: 54) and around 11,000 residential units traded (Q1/2025: 17,000). In terms of the number of transactions, this is the strongest first quarter since the interest rate shock in 2022.

The decline in transaction volume is mainly due to structural shifts. The five largest transactions of the quarter represented only 38 percent of the total volume (620 million euros), while their share in the same quarter of the previous year was still 52 percent (1.21 billion euros). The average transaction size fell to EUR 29 million in the first quarter (previous year: EUR 44 million). This continues the trend from previous years: In 2024, an annual average deal size of 41 million euros per transaction was observed, in 2025 this fell to 35 million euros.

“The higher number of transactions shows that the market remains active. At the same time, however, geopolitical uncertainties are clouding the investment climate somewhat,” comments Michael Bender, Head of Residential JLL Germany.

Core transactions accounted for 46 percent of the total volume, compared to 54 percent in the prior-year quarter. The core-plus risk class has a share of 33 percent, while value-add transactions have the highest value in several quarters at around 20 percent. “This could indicate an increasing risk appetite of individual investors or improved price discovery in the value-add segment,” analyzes Helge Scheunemann, Head of Research at JLL Germany.

Metropolises are still underrepresented

The markets in the seven metropolises are still rather underrepresented. Their share of the total volume was 41 percent in the first quarter of 2026, compared to 38 percent in 2025 as a whole. This means that the share of sales in the metropolises is still well below the five-year average (57 percent).

Within the metropolises, Hamburg accounts for the largest share of the pie at 27 percent – a significant increase compared to two percent in the same quarter last year. One of the reasons for this is one of the larger transactions of the quarter, in which Quantum’s saga acquired land and turnkey properties on the Holsten site with a volume of around 700 subsidized apartments. Berlin follows in second place with a share of 15 percent (250 million euros).

Forward transactions remain important – municipal buyers remain active

Forward transactions retained their importance and accounted for about 37 percent of the transaction volume (610 million euros in 13 transactions). The average size of forward deals was around 47 million euros, well above the overall market average. On the buyer side, municipal and state-owned housing companies such as Saga, the housing companies of the city and state of Berlin, Gesobau or Degewo were the dominant group of buyers. Around 54 percent of the forward transactions had a subsidized share of housing, and within this group, the share of subsidized housing units is around 84 percent on average.

Prime yields in the seven largest cities remained at an average of 3.51 percent in the first quarter of 2026. Due to lengthy transaction processes, changes in the capital market only became apparent with a time lag. The yield delta between good and medium quality properties remained at the previous year’s level at 50 basis points.

Declining affordability slows down rent development

Meanwhile, the German rental housing market remains characterized by considerable tensions. This is due to the sharp rise in new contract rents in recent years – both in new buildings and in existing buildings. Despite high nominal wage increases, the proportion of income that has to be spent on housing costs is steadily increasing. “Affordability is increasingly becoming a limiting factor for rent development,” says Dr. Sören Gröbel, Director of Living Research at JLL Germany. “The shortage of affordable and social housing is particularly noticeable.”

Although there were signs of a slight recovery in new residential construction, the consequences of the Iran war with expected rising construction costs and interest rates as well as more difficult interest rate hedging are slowing down this trend. “In particular, interest rate hedging for project developments has become more expensive and complex due to geopolitical events such as the Iran war, which further inhibits the realization of urgently needed construction projects,” explains Gröbel.

Iran war and energy prices weigh on capital market environment

The capital market environment in the first quarter of 2026 was shaped by the Iran war and sharply increased energy prices. Inflation in the eurozone jumped to 2.5 percent in March, and in Germany even to 2.7 percent – mainly due to the abrupt increase in energy costs of 4.9 percent year-on-year. The interest rate market reacted clearly: the five-year swap climbed by 65 basis points to 2.99 percent, mortgage rates with a ten-year maturity rose by 38 basis points to over four percent.

“Geopolitical developments have noticeably worsened financing conditions. The disproportionate increase at the long end of the yield curve indicates growing uncertainty,” explains Scheunemann.

The fragmentation of the market and the concentration on core and core plus products is likely to continue in the short term. A revival of the residential investment market depends on improved price discovery, especially in the value-add segment, as well as more stable financing conditions.