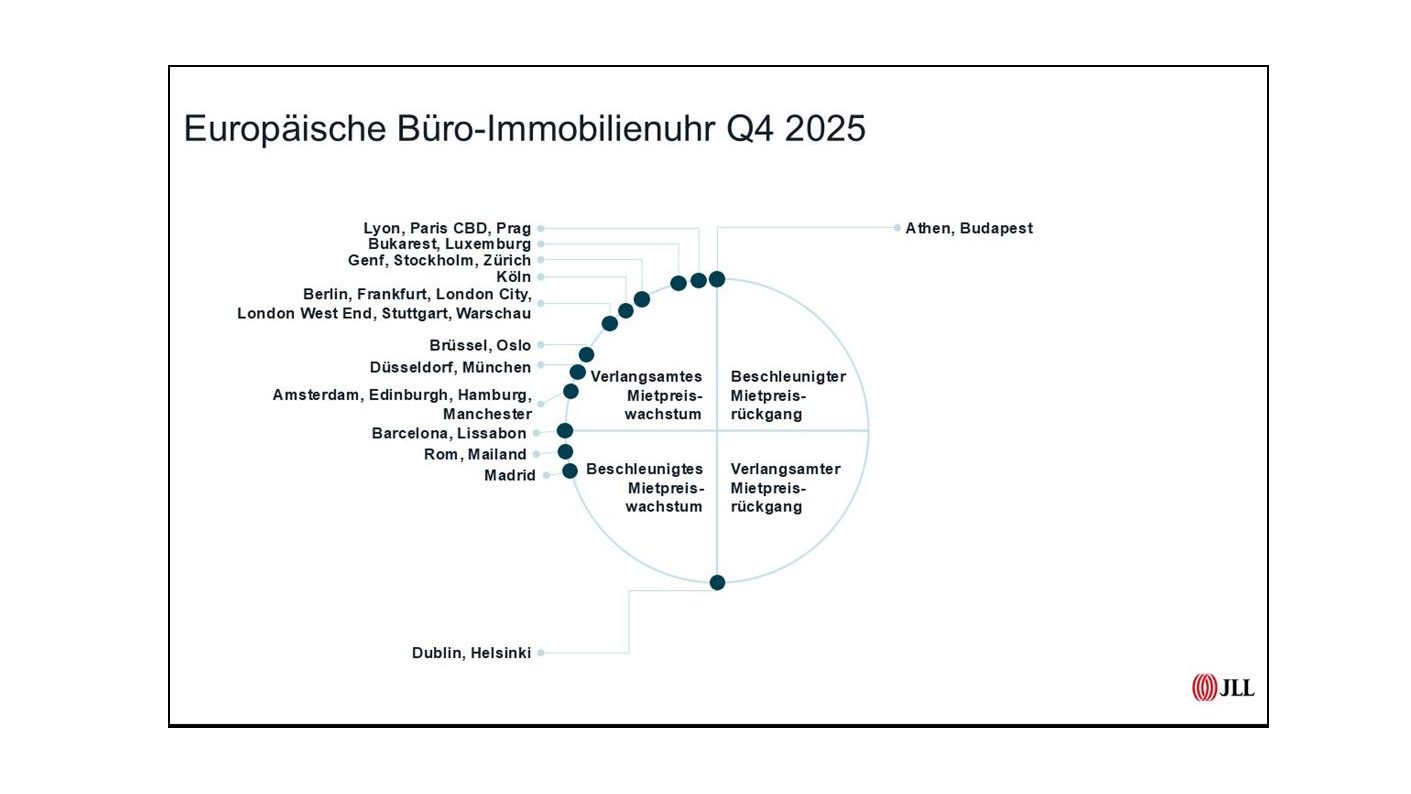

JLL EMEA office real estate clock in the fourth quarter of 2025

The clock shows where JLL expects the office markets to be within their rental price cycles at the end of December 2025. The local market can move in different directions and at different speeds in the clock. The clock is a method of comparing the positions of the markets in their cycle. The positions are not necessarily representative of the investment and project development market. The positions of the markets refer to prime rents. There are markets that do not follow a conventional cycle and tend to move between 9 a.m. and 12 p.m. In this case, 9 a.m. represents an increase in rents after a period of rent stability.

- The European office rent index rose by 7.4 percent year-on-year in the fourth quarter of 2025 and by 1.7 percent quarter-on-quarter.

- Take-up reached around 2.3 million m² in the fourth quarter of 2025. This is an increase of ten percent compared to the third quarter of 2025, but minus eight percent year-on-year.

- Europe’s office vacancy rate rose by a total of 60 basis points to 9.3 percent over the course of 2025, but is expected to stabilize by the end of 2026.

- Completions amounted to 891,000 m² in the fourth quarter and around 3.5 million m² in 2025 as a whole. That is 17 percent less than the ten-year average.

The fourth quarter of 2025 was relatively stable despite some economic challenges. Tariff uncertainty decreased, bond yields remained elevated but controlled, and while the war in Ukraine continues, an official ceasefire is in place in Gaza. The French government persevered without passing a budget, and the British budget was well received by the public and the business community.

The economic development was rather modest. Although a recession was avoided, growth remained low. EU industrial production rose by 2.2 percent year-on-year in December, with German production bottoming out and returning to positive growth. France’s economy performed positively throughout the second half of the year, while the UK recorded an industrial recovery in November.

The purchasing managers’ indices (PMI) in the manufacturing sector pointed to minor changes compared to the previous months. In contrast, services in the major economies lost some momentum. As a result, eurozone GDP growth slowed to 0.2 percent in the fourth quarter compared to 0.3 percent in the third quarter, impacted by weaker French growth and German stagnation.

The European Central Bank (ECB) has been maintaining its exchange rate policy since June. In the future, too, hardly any change in the interest rate level is expected. The inflation rate in the eurozone reached the target of two percent in December and is expected to remain close to this target throughout 2026.

“Low key interest rates, contained inflation and rising household spending items in 2026 suggest a slight to good economic development, although US trade and security policy poses significant risks,” says Hela Hinrichs, Senior Director Research & Strategy JLL EMEA, analysing the economic outlook.

Prime office rents: Only in just under half of the metropolises is the price screw turning

European prime office rents rose by 7.4 percent year-on-year and by 1.7 percent quarter-on-quarter in the fourth quarter of 2025, remaining above the ten-year average.

As expected, the increased rents are increasingly playing a role in the location decision and motivating users to consider space outside the central prime locations. Therefore, rental growth is expected to extend from prime office space in central locations as competition in A-locations increases. “The Paris business center is a good example of this. ” The market has reached record rents and growth is expected to flatten out or even possibly turn negative by the end of 2026,” says Hinrichs.

Rent increases were observed in eleven of the 23 index markets, including Hamburg (up 13.9 percent quarter-on-quarter), Madrid (up 3.5 percent), Edinburgh (up 3.3 percent), London (up 2.9 percent) and Rotterdam (up 2.9 percent). The remaining twelve markets did not record any rental growth in the fourth quarter.

Take-up ranges from plus 207 per cent to minus 85 per cent

Office space take-up in Europe reached around 2.3 million m² in the fourth quarter of 2025. This is a decline of eight percent year-on-year, with the weakness mainly due to German cities and Paris. Political and economic challenges are causing many companies to postpone their location decisions.

The market development in Europe is very different: Ten index markets recorded an increase in take-up compared to the previous year – led by Rotterdam (plus 207 per cent), Dublin (plus 56 per cent) and Budapest (plus 39 per cent). In contrast, sales declined in twelve markets, including The Hague (minus 85 percent), Edinburgh (minus 66 percent) and Lyon (minus 46 percent).

Comparing the regions with each other, take-up in Central and Eastern Europe fell by eight per cent year-on-year to 230,000 m² in the last quarter of 2025. In Western Europe, too, the figure fell by eight percent to a total of 2.1 million m².

Over the year as a whole, Frankfurt (up 53 percent), Amsterdam (up 39 percent) and Luxembourg (up 38 percent) saw a significant recovery in demand. London also reports growth of ten percent for 2025, while Europe’s largest market Paris suffered a decline of nine percent. Germany’s five largest stores enjoyed stable leasing activity and registered a total of 2.3 million m² of office space in 2025 (up 0.5 per cent).

Despite the subdued momentum in the second half of the year, sentiment is improving. Since many leases from 2017 and 2018 expire in the medium term, demand is likely to increase in 2026. However, the limited supply of high-quality space and the lack of available new construction space will limit sales growth.

Vacancy rate to increase by 60 basis points in 2025 and expected to stabilise in 2026

The European vacancy rate rose to 9.3 percent in the fourth quarter of 2025, an increase of 60 basis points year-on-year. “However, we assume that the rate is expected to stabilize by the end of 2026 and will not increase further due to declining new construction volumes,” Hela Hinrichs expects. It is noteworthy that in Central and Eastern Europe, the trend was reversed: the vacancy rate here fell by 150 basis points year-on-year, from 10.8 percent to 9.3 percent.

The individual markets also developed very differently: Twelve index markets recorded year-on-year vacancy increases, led by Munich (up 210 basis points to 8.5 percent), Amsterdam (up 180 basis points to 9.8 percent) and Hamburg (up 140 basis points to 6.7 percent). Conversely, ten markets marked declines, in particular Dublin (minus 280 basis points to 13.0 percent), Barcelona (minus 170 basis points to 8.8 percent) and Budapest (minus 160 basis points to 12.5 percent).

European property developers are reacting to the historically high vacancy rate by scaling back their construction projects. The number of office space under construction fell to 9.9 million m² across Europe. This is eleven percent less than in the previous year and around 13 percent below the average of the past decade. London and Paris, as well as Berlin, Munich, Frankfurt, Hamburg and Düsseldorf, together account for 60 percent of construction activity in Europe, with the German markets recording the sharpest year-on-year decline at 21 percent.

Completions in the fourth quarter totalled 891,000 m², bringing the total office space for 2025 to 3.5 million m². This is 16 percent less than the average of the past decade.