According to analyses by “DIP – Deutsche Immobilien-Partner”, the German retail market achieved a new nominal record turnover of around EUR 677 billion in 2025 (2024: around EUR 664 billion). According to investigations by the German Retail Association (HDE), online retail increased by around 4.5% to approx. EUR 92.4 billion (2024: approx. EUR 88.4 billion) and thus also reached a new record.

At the same time, the prime rent for top retail space, averaged across all locations analysed by DIP, remained stable. In the individual markets, however, there were differentiated developments.

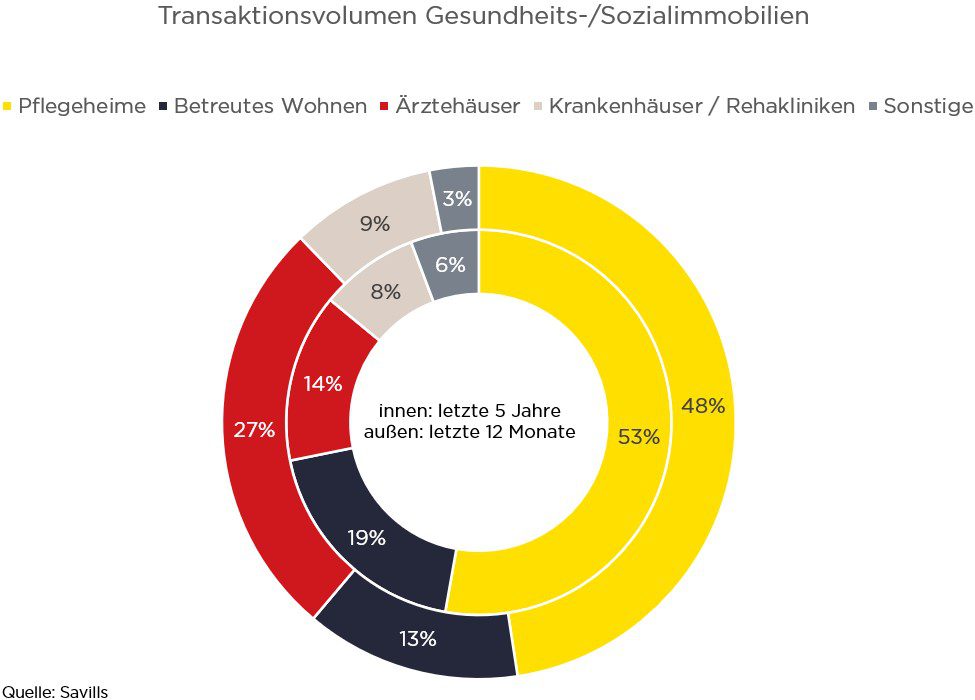

Investments in retail real estate increased compared to the previous year.

Notwithstanding the increased sales figures, it can be said that economic stagnation in 2025 will continue to weigh on the retail sector in Germany. The background to this is the following factors:

- The real wage index rose by around 2.0% on average for the year, but was only able to partially compensate for the loss of purchasing power in previous years.

- The unemployment rate rose slightly to 6.1% on average for the year, an increase of 0.1 percentage points compared with the previous year. The number of unemployed thus stands at an annual average of 2.82 million, accompanied by a decline in labour demand, which in 2025 reached its lowest level in the last 20 years.

- Consumers’ propensity to save declined slightly, and the consumer climate showed a moderate recovery at the end of the year, but remained at a very low level of -21.3 points. The GfK/NIM consumer climate index fell again compared to the previous year and stood at around -23.4 points at the end of 2025 (end of 2024: -21.3) and deteriorated to -26.9 at the beginning of 2026.

- Continued high food and energy prices, which reduced real disposable income despite declining inflation, and increasing concerns about job losses as a result of relocations, production cuts and announced closures in key industrial sectors had a particularly negative impact.

- The long-term developments in brick-and-mortar retail can also be seen in the number of stores: According to HDR analyses, there were still around 372,000 stores nationwide in 2015, but by 2025 their number had fallen by 19% to just around 372,000 stores. 301.500. According to HDE forecasts, this trend will continue.

Differentiated development of retail sales.

Despite this difficult starting position, the retail sector was able to post a new record turnover of around EUR 677 billion in 2025. In nominal terms, this result represents an increase in turnover of 2% compared to 2024 (approx. EUR 664 billion). In price-adjusted terms, however, real turnover was only 0.2% higher than a year earlier, partly due to inflation.

In terms of sales development, a distinction must be made between stationary and online retail:

- After online retail sales jumped by around 47% from around EUR 59 billion in 2019 to just under EUR 86.7 billion in 2021 during the pandemic, according to analyses by the HDE, its growth was halted in 2022 for the first time in years and fell by -2.5% to EUR 84.5 billion. In 2023, this trend was reversed with an increase to around EUR 85.4 billion and continued in 2024 with a nominal increase of 3.4% to around EUR 88.4 billion. In 2025, sales rose again by around 4.5% to EUR 92.4 billion.

- Turnover in stationary retail (other retail trade with goods of various kinds; e.g. department stores) increased by around 1.6% year-on-year to around EUR 585 billion (2024: around EUR 576 billion).

Differentiated development of the prime rent level.

In 2025, the average prime rent in the markets analysed by DIP remained stable compared to the previous year at EUR 173/m², but remains well below the value of 2022 (EUR 179/m²). In doing so, DIP analyzes different rental developments:

- While prime rents in Frankfurt rose by EUR 5/m² and in Dresden by EUR 10/m² and in Freiburg and Karlsruhe by EUR 15/m² each, they fell in Berlin (- EUR 10/m²), Nuremberg (- EUR 28/m²) and Essen (- EUR 5/m²). In the other locations, DIP is recording stable prime rents.

- In the “Big Seven” Berlin, Düsseldorf, Frankfurt, Hamburg, Cologne, Munich and Stuttgart, the average prime rent remains unchanged at around EUR 271/m².

- In the remaining nine markets, the average prime rent for 1A locations is slightly above the previous year’s figure at around EUR 97/m² (2024: around EUR 96/m²).

- The highest prime rents continue to be achieved in Munich at EUR 340/m², followed by Berlin (EUR 300/m²), Düsseldorf (EUR 275/m²) and Frankfurt (EUR 270/m²).

The developments in the individual markets shown, from significantly increased prime rents to stable prices and further rent declines, show the heterogeneity of the German retail trade in view of its polycentrality.

Prospects and investment opportunities

In the retail investment market, cash turnover in 2025 increased by around 10% year-on-year to around EUR 6.44 billion (2024: around EUR 5.84 billion). A positive development was particularly visible in the A locations. The focus was primarily on Munich and Berlin with significant transactions. The other A-cities recorded a comparatively restrained, but also increasingly stable upward trend.

- At the same time, the average prime yield in the 16 markets analysed for commercial buildings in top city locations has risen moderately by 10 basis points to currently 4.7% p.a., while it is stable at 6.1% p.a. for hypermarkets and specialist stores.

- For 2026, demand is expected to continue to be strongly concentrated on retail park and food-anchored investments as well as corresponding portfolio solutions. High-street locations with high footfall and established luxury locations in economically strong locations also remain in high demand. However, these investments react sensitively to price and interest rate developments, so that transactions are carried out primarily with attractive risk-return profiles. The market launch so far indicates a stable development, especially of prime yields in 2026.