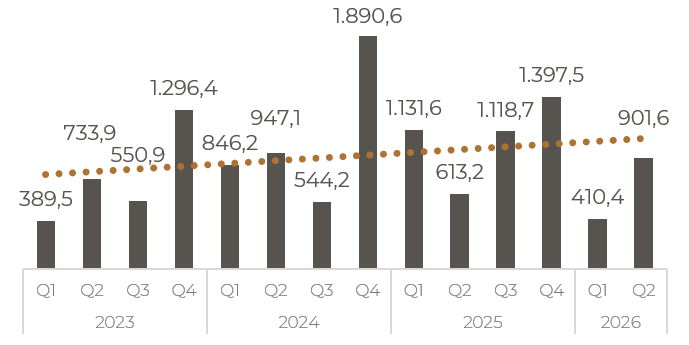

The German office markets have made a moderate start to the new year overall. In Germany’s most important office strongholds of Berlin, Düsseldorf, Essen, Frankfurt, Hamburg, Cologne, Leipzig and Munich, take-up in the first quarter of 2026 amounted to 603,000 m², which corresponds to a year-on-year decline of -14%. However, the markets of Berlin and Munich are setting strong accents in a continuously challenging market environment, with sales growth of 42% and almost 26% respectively. This is the result of the analysis by BNP Paribas Real Estate.

The most important results at a glance:

- At 603,000 m², take-up around 14% below the previous year’s level

- Vacancy rate rises to 8.9 million m² (+11% year-on-year)

- Construction activity stable at the beginning of the year at a low 2.2 million m² (-6% year-on-year)

- Prime rents in Frankfurt, Hamburg and Munich continue to rise in the first quarter

“At the beginning of 2026, the German office markets are under the impression of a persistently weak economic development and an unchanged fragile geopolitical situation. It was therefore not possible to build on the accelerated start to 2025 with the now registered take-up of 603,000 m². However, the minus of 14% is comparatively moderate in view of the large number of major trades that signalled in the previous year. The markets are being driven by brisk leasing activity in the smaller space segment and increasing momentum in medium-sized deals. They will be raised above the previous year’s level and the average of the past five years if major contracts have been successfully concluded and significantly more movement can be registered in deals between 5,000 and 10,000 m²,” explains Marcus Zorn, CEO of BNP Paribas Real Estate Germany. “It is precisely these major deals that have now raised the markets in Munich and Berlin to their current level, with which they clearly leave the field of locations behind. However, all markets have one thing in common: the tenants’ demand pattern for smaller but higher-quality office space has become entrenched. Large international companies in particular show little willingness to compromise when it comes to space and location quality. The search for adequate offices in premium locations can be time-consuming due to the lack of vacancies and also require creative solutions. Despite these challenges, we have been registering a stable level of large contracts for several months. A strong signal from all market participants to take account of new space requirements – whether in renting or letting.”

Munich and Berlin lead the way with strong sales growth, Hamburg in 3rd place by far

With take-up of 172,000 m² and take-up of 25.5% compared to the start of 2025, Munich has impressively taken the lead among Germany’s office strongholds. As in the previous year, the Bavarian capital was able to register three major deals in the first three months of the year. The deals of E.ON SE and the software developer JetBrains, each comprising more than 20,000 m² of rental space, are sending particularly strong signals to the market. Both the application by E.ON SE, which was successfully supported by BNP Paribas Real Estate, and that of JetBrains were implemented in highly attractive areas on the outskirts of the city. In addition, leasing activity in Munich accelerated, especially in the size class between 2,000 and 10,000 m², and made a decisive contribution to the result. The mid-size segment is then also the sales driver in Berlin, with a current above-average market share of 38% and a tripling of sales compared to the previous year. Together with Strabag’s major deal (12,000 m² of rental space), they raise take-up in Berlin to 146,000 m², or an increase in take-up of almost 42%. Hamburg follows at a considerable distance with 91,000 m² of take-up (-18%).

Frankfurt ranks 4th with 82,000 m² of take-up. Not entirely unexpectedly, the market in the banking metropolis is unable to match the brilliant record turnover at the start of 2025 and falls short of it by almost 60%, although another major transaction was made with DZ Bank’s owner-occupier deal in Fifty Avon with almost 21,000 m². DZ Bank’s choice of space and location once again clearly illustrates what is driving the market in Frankfurt, but also in the other German office strongholds: a strong demand for premium space in top locations that cannot be adequately served in the short term, so that the decision on space for project developments remains the best alternative. New leases are often accompanied by location consolidation. DZ Bank will comprehensively modernize the tower acquired next to its headquarters and center various corporate units here in an attractive banking location.

Once again, the office markets of Cologne and Düsseldorf are at a similar level. While Cologne missed the previous year’s result by around 33% at 45,000 m², the Düsseldorf market grew by 8% to 42,000 m² at a low level. The start of the year was disappointing in Leipzig (15,000 m²; -6 %) and Essen (10,000 m²; -63 %).

Vacancy rate rises to 8.9 million m² – but growth continues to lose significant momentum

The vacancy rate in the office strongholds analysed amounts to a total of 8.9 million m². This is an increase of 11% compared to the same quarter of the previous year. However, the development in the past three months shows that the increase in vacancy rates is clearly slowing down and that the first markets are reaching the peak. The vacancy rate in Leipzig is a low 5.8% nationwide and is only slightly higher in Hamburg (6.4%) and Cologne (6.5%). Munich ranks with 8.0%. In Essen, 8.9% are registered. Beyond 9%, the vacancy rate is recorded in Berlin (9.1%), Frankfurt (11.7%) and Düsseldorf (12.6%).

While the vacancy rate is at a high level, especially in the segment of older existing buildings and in less well-connected locations, the lack of first-time occupancy space available at short notice in premium locations remains glaring. In total, the volume in this location and quality segment in the markets analysed amounts to just under 65,000 m², which corresponds to a decline of 4% in the first quarter alone and underlines the excess demand here. In Berlin, Düsseldorf, Essen and Cologne, the vacancy rate in the top segment remains well below the 5,000 m² mark. For all office strongholds, large-volume space requests in the absolute premium segment can currently only be met within the framework of project developments.

Construction activity stable at the beginning of the year at a low 2.2 million m²

With a volume of around 2.2 million m², construction activity remains at a very low level. While a decline of around 6% compared to the previous year is registered, a sideways movement can be reported for the first months of the year overall. The shortage of vacant premium space is keeping pre-letting rates in all markets at a high level or causing them to rise further, as large-scale space searches in the top segment in particular can currently only be realised in project developments. In Berlin, the pre-letting rate (18.9%) is slowly heading towards the 20% mark at a low level, while in the majority of cities it is above 50%, with a peak of almost 73% in Cologne.

The key figure for the office market in terms of available space (vacancy rate and space still available under construction) remains almost unchanged at 10.15 million m².

Prime rents in Frankfurt, Hamburg and Munich continue to rise in the first quarter

The lack of vacancies in the premium segment and the need to be able to implement large-scale top requests only in project developments is keeping the pressure on prime rents high. Prime rents continued to rise in Frankfurt, Hamburg and Munich in the first quarter. In Frankfurt and Hamburg, it rose by €1.00/m² each to €55.00/m² and €39.00/m² respectively. For Munich, an increase of €1.50/m² to currently €59.50/m² is reported. The Bavarian capital thus remains the most expensive office location in Germany and its rent level is heading for €60/m² at its peak. Prime rents in Berlin (€47.00/m²), Düsseldorf (€46.00/m²) and Cologne (€33.50/m²) are stable at a high level, followed by Leipzig (€21.00/m²) and Essen (€20.00/m²).

The more volatile average rent in the majority of markets continues to trend upwards at the beginning of the year. At €27.30/m² each, the average rent in Frankfurt and Munich is currently the highest. Berlin follows at a small distance with €27.00/m². The average rent is also above the €20/m² mark in Düsseldorf (€22.00/m²), Hamburg (€22.10/m²) and Cologne (€21.40/m²). A significantly low rent level is reported for Essen (€13.80/m²) and Leipzig (€13.50/m²).

Prospects

The German office leasing markets are once again starting a new quarter under a stressful environment. In view of the armed conflicts in the Middle East, economic expectations have deteriorated noticeably and, according to GfK, ifo and ZEW, the mood of consumers, entrepreneurs and financial market experts is also much more pessimistic at the end of March than in February. There is little to suggest that the German economy will provide the sustainable tailwind on the office markets in the further course of the year that was forecast just a few months ago. At the moment, the possible effects on the global economy due to the Strait of Hormuz, which is currently hardly passable, seem too burdensome. Nevertheless, Germany’s largest office markets are heading for a year that will be stable compared to the previous year and probably even stronger in terms of turnover, as the markets have a sustainable underlying dynamic. The continued brisk leasing activity in the small space segment is increasingly being supplemented by an increased frequency of medium-sized leases. In addition, there are the large-scale searches that have been initiated over many months and should be successfully implemented in the coming months.

“The economic conditions remain challenging for the time being and uncertainty about the economic development is high. This makes it all the more important to look at the fundamentals of the office leasing market. After a profound structural change in user behaviour, the demand for office space is picking up again. Unlike in previous years, it is more focused and quality-oriented. Users are looking for modern, sustainable and representative spaces that meet their requirements in terms of efficiency, location and employer attractiveness. Where such space is lacking in the short term, decisions often shift to project developments, repositioning or comprehensively modernised properties. In our view, this suggests selective but resilient market activity for the remainder of the year. Although a rapid revival across the board is not the most likely scenario, there is an increasing closing momentum in the marketable segments while at the same time continuing high rental pressure in the top segment,” summarizes Marcus Zorn.