The momentum on the German office property market will continue to be subdued in the first quarter of 2025. Transactions and lettings remain below the long-term average. But beneath the surface, movement is beginning to emerge – especially in indirect investments. Here, several catalysts ensure that volumes are likely to increase in the medium term.

Standstill agreements expire, selling pressure increases

In recent years, standstill agreements have been concluded in many institutional portfolios, especially in Depot A structures of banks and savings banks. These prevented larger sales of fund units for the time being. Now, however, many of these agreements are expiring – and with them the number of banks that want or need to realign their portfolios is growing. Office real estate funds are particularly affected by this new selling pressure, as their properties (as mentioned at the beginning) often no longer correspond to their original core character. This applies in particular to buildings in good locations that were bought at top prices years ago, but are no longer competitive today in terms of ESG, rentability or location – but this is potentially becoming the case again through targeted manage-to-core approaches.

Special situations and trophy properties come into focus

In addition, there are special situations that further change the picture. Owners are increasingly starting to place prestigious properties – so-called trophy buildings – on the market. The most prominent example is the “Upper West” in Berlin, which went to the Schoeller Group in January 2025 for around 450 million euros. In the process, the buyer side converted part of an earlier financing to Signa into equity – an example of a transaction with an impact on the balance sheet instead of a classic asset deal. As a result, not only are corresponding individual transactions offered more frequently, but also fund units with office exposure on the secondary market – often discreetly and within the framework of structured processes.

Pricing remains challenging – opportunities for selective buyers

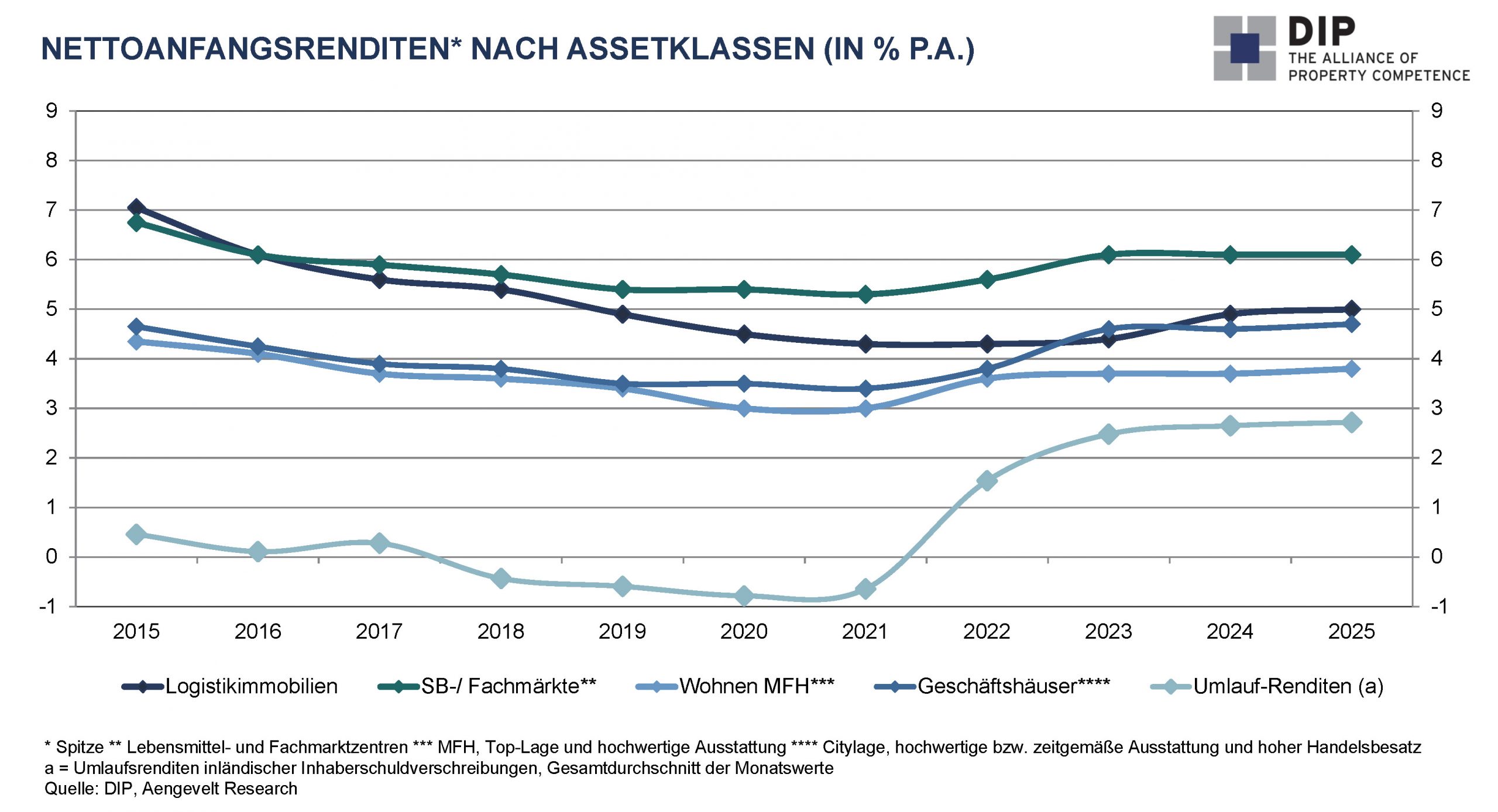

The central challenge remains pricing. Although the differences between buyers and sellers have narrowed, there are still different return expectations. While sellers in the recent past were still guided by earlier market values, the more realistic market assessment is becoming more and more prevalent. Currently, many investors are now aiming for net initial yields of 5.5 to 6.0 percent (for office funds) – well above the level of recent years.

This is hardly feasible with the income of classic core offices. Consequently, sales can only be realized through significant price discounts. This is precisely what investors who are willing to invest in more management-intensive properties with development potential – whether through repositioning, ESG upgrades or realignment of the rental structure – are aiming for. Of particular interest are shares in funds where they can take control and where institutional sellers want to exit for strategic reasons without liquidating the fund itself.

The secondary market for special fund units offers institutional investors a discreet opportunity to sell investments – without interfering with the fund structure. Especially for banks and pension funds, this is a practical way to adjust office allocations without triggering operational consequences. The processes are increasingly standardized, legally secure and efficient – an advantage over open terminations, which can lead to structural market distortions.

Outlook: The window of opportunity opens

The German office investment market is still far from normalizing. But the conditions for more activity are increasing: selling pressure meets growing opportunities, institutional sellers are signalling an increasing willingness to take action, and structural changes – from ESG obligations to refinancing pressures – are acting as additional catalysts.

For selective investors with experience and perseverance, there is now an interesting window of opportunity. Those who are willing to examine even more complex constellations can return to the market at attractive entry conditions. The decisive currency is not only capital, but also flexibility and transaction security.