In 2025, Germany once again recorded a record number of overnight stays with 497.5 million overnight stays. As in the previous year, this positive development was driven by robust tourism demand. Against this backdrop, the hotel investment market has also continued to stabilize. At the beginning of 2026, demand for overnight stays continued to develop moderately positively. Domestic demand in particular has risen recently; foreign demand, on the other hand, increased only slightly.

“For the hotel industry in Germany, this means that the demand base remains solid, but the operating performance is no longer driven solely by catch-up effects or major events,” says Martin Schaller, Head of Asset Management Hospitality at Union Investment, explaining the latest results of the market analysis carried out together with bulwiengesa. In contrast to 2024, when, among other things, the trade fair and congress business as well as major events such as the European Football Championship significantly supported the occupancy rate of the city hotel industry, since 2025 the sustainable earnings quality of the businesses has come more to the fore. “Real sales growth, rising costs, differentiated location developments and the quality of operator concepts are thus becoming increasingly important for the valuation of hotel properties,” says Martin Schaller.

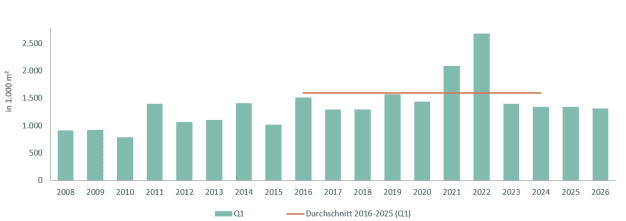

Hotel transaction market with revival

In this dynamic market environment, transaction activity picked up significantly in 2025. The final transaction volume for the full year 2025 in Germany amounted to around EUR 1.9 billion, roughly on a par with the average level of the years 2020 to 2024, an increase of more than a third compared to 2024. The market was primarily driven by large-volume individual transactions, which accounted for about three-quarters of all transactions. At the same time, strategic portfolio deals are making a comeback.

Prime yields in the German hotel segment were stable to slightly declining overall in 2025 compared to 2024. While the German average remained at around 5.25 percent, the significant increase in market liquidity, larger transactions and the return of core and core-plus investors in selected prime locations led to a moderate downward pressure on prime yields. However, there is no discernible nationwide yield compression; rather, pricing remained strongly dependent on the property, location, operator and contract.

Almost 10,000 new rooms – hotel value rises by around 2.8%

“Against this backdrop, the positive performance trend of German hotel properties remains intact, although the momentum has weakened compared to the previous year,” says Dr. Joseph Frechen, Head of Division at bulwiengesa. According to the calculation, which was carried out together with Union Investment, a moderate increase in value of around 2.8 per cent was determined for the investment-relevant hotel market segment on the basis of data on market development and the operating performance of the hotel businesses.

Based on an investment-relevant hotel market volume of EUR 64.3 billion in 2024, a volume of around EUR 66.1 billion was calculated for 2025. While the values of the existing hotels increased only slightly by around 0.5 percent across all locations and market segments, the largest part of the increase in value comes from the completion of new rooms. According to the evaluation of the bulwiengesa databases, almost 10,000 rooms in the investment-relevant hotel segment were completed and launched on the market in 2025. “This results in an additional market volume of around EUR 1.5 billion,” says Dr. Joseph Frechen.

Focus of new openings outside the A-cities

It is noteworthy that the high-end luxury and upper upscale segments were less strongly represented in new openings in 2025 than the lower-priced economy and midscale segments. Accordingly, the increase in value from newly opened rooms fell short of the momentum of 2024. In addition, only around 20 percent of the new opening volume was concentrated in the A cities; the larger part was accounted for by smaller towns and rural tourism regions. “This underlines the efforts of the hotel groups to build up broader market penetration with their brands and to tap into demand potential beyond the established metropolises,” says Martin Schaller.

Transformation and conversion projects continue to gain relevance

According to data from the bulwiengesa Development Monitor, transformation and conversion projects accounted for around a third of the new hotel rooms coming onto the market in 2025. The development focus was particularly on the midscale and upscale segments; at the same time, high-quality repositioning was also implemented in the Luxury segment. Examples of this are the “Conrad Hamburg” in the Levantehaus and “The Florentin” in the former Villa Kennedy in Frankfurt. Serviced apartment operators and hybrid accommodation brands also appear as active users of existing properties. In particular, providers such as “STAYERY” and “limehome” are using former hotels, office buildings and mixed-use properties for new apartment and long-stay concepts. In addition, projects currently being implemented, such as those of the Ruby brand or “The Cloud One”, show that lifestyle and lean luxury brands are also focusing specifically on revitalisation, conversion and architectural identity.

“It is striking that transformation and conversion projects are particularly implemented in A-cities, while cities outside the large metropolises are less represented,” explains Dr. Joseph Frechen. “In the A-cities, the projects are also predominantly positioned in a high-quality position. Midscale, upscale, upper-upscale and luxury concepts dominate here; pure economy projects do not play a decisive role in this group of transformation and renovation projects.”

A major reason for this development is the limited availability of space for classic new hotel buildings in A-cities. Central plots of land are scarce, expensive and often already built. “New hotel capacities are therefore increasingly being created through revitalization, repositioning and conversion of existing properties,” says the bulwiengesa expert. At the same time, A-cities are characterized by high tourism and business demand, strong MICE and corporate demand, international brand presence, a professional operating environment and high liquidity in the investment market. These location qualities justify higher investments in renovation, gutting, technical upgrading and design upgrade. “In A-cities, renovations and conversions are not only a reaction to a lack of new construction space, but often also an instrument for the value-enhancing repositioning of existing properties,” says Martin Schaller.

For 2026, bulwiengesa and Union Investment expect room growth at at least the same level and thus a continuation of the conversion trend.