Hamburg and Düsseldorf impress in the first half of 2026

In the seven largest German cities, commercial real estate worth 6.5 billion euros was acquired in the first half of the year, an increase of around ten percent year-on-year. The second quarter accounted for 3.35 billion euros, slightly more than in the first quarter (3.15 billion euros).

The individual cities were very heterogeneous. While Hamburg recorded a remarkable increase of almost 60 percent with a transaction volume of around 1.59 billion euros in the first half of the year, Stuttgart with 180 million euros remains far behind the previous year’s figure and the long-term averages. Foreign investors acted as net sellers in six of the seven metropolises, reducing inventories totalling 420 million euros.

Logistics prime yields stabilized between 4.5 and 4.6 percent, while office yields rose by 10 to 20 basis points in all cities. Major deals over 100 million euros gained in importance: In Düsseldorf, 68 percent of the volume was accounted for by three such transactions.

")

Berlin recorded a transaction volume of 1.63 billion euros in the first half of 2026, a decline of 16 percent compared to the same period last year and 63 percent compared to the ten-year average. The prime office yield rose from 4.2 to 4.4 percent, retail remained at 3.4 percent, logistics at 4.6 percent. Foreign buyers accounted for 51 percent of the shares and built up a net portfolio of 96 million euros. The five largest deals accounted for 37 percent of the volume, while three transactions in the three-digit million range generated 420 million euros.

Anja Schuhmann, Branch Manager Berlin & Leipzig: “Despite a decline compared to the previous year, Berlin maintains its top position among German investment metropolises in terms of transaction volume. In view of the conflict in the Middle East, there has been no recovery in the transaction markets. Investors remain highly selective, purchase processes protracted, banks cautious, and the market environment remains fragile due to geopolitical uncertainties. However, the decisive factor is that liquidity is available for a very good product in Berlin’s top locations, and the current pipeline is promising.

A strong signal for the location is the coalition decision of the Union and SPD, which opposes the nationalization of private rental housing stocks through socialization laws at the state level. This creates important investment security, stabilizes framework conditions and mobilizes private capital – exactly what Berlin needs to create significantly more housing again.”

At 1.03 billion euros, Düsseldorf exceeded the previous year’s result by 37 percent, but is 18 percent below the ten-year average. The prime office yield rose to 4.7 percent, retail remained at 3.6 percent, logistics at 4.6 percent. German investors dominated on both sides with over 74 percent, while foreign players reduced a net of 20 million euros. Three deals worth 100 million euros totaled 700 million euros, which corresponds to 68 percent of the total volume. Office properties played a central role with around 37 per cent, while mixed-use and logistics properties contributed 27 per cent and 24 per cent respectively.

Marcel Abel, Managing Director and Branch Manager JLL Düsseldorf: “Düsseldorf’s investment market is showing remarkable strength in the first half of 2026, making it one of the most dynamic markets among the seven metropolises. This development reflects what we already identified as a trend reversal at the end of 2025: the price discovery phase is largely complete, institutional investors are noticeably returning to the market. Düsseldorf is benefiting in particular from its stable user base and growing demand for first-class office properties in central locations. We expect this momentum to continue in the second half of the year, provided that the interest rate environment does not provide any new disruptive impulses.”

At 530 million euros, Frankfurt reported its weakest first half of the year in years. The result is around 20 percent below the previous year and 79 percent lower than the ten-year average. The prime office yield climbed to 4.8 percent, retail is unchanged at 3.5 percent and logistics at 4.5 percent. Foreign investors reduced their positions by 210 million euros net. The five largest transactions accounted for 56 percent of the volume. German buyers were dominant with 76 percent. Office properties were the dominant type of use with around 48 percent, followed by residential and logistics properties with 27 percent and 18 percent respectively.

Suat Kurt, Branch Manager JLL Frankfurt: “The Frankfurt office investment market continues to tread water in the second quarter. Although the transaction volume after the first half of the year is already almost at the level of 2025, only a very small number of deals were recorded in the second quarter. There is still a lot of product on the market, but the processes are still dragging on and the abandonment rate remains high. Nevertheless, we expect transaction activity to continue to rise at a low level.

Meanwhile, the Frankfurt residential investment market continued the development of the start of the year in the second quarter. Transaction activity continues to move at a growing level, with investors maintaining their selective approach. Market participants are acting prudently and focusing on high-quality properties in established locations.”

Hamburg shone with 1.59 billion euros, an increase of 59 percent compared to the previous year and only two percent below the five-year average. The prime office yield rose to 4.25 percent, retail remains at 3.4 percent, logistics rose to 4.5 percent. Foreign investors reduced stocks of 180 million euros net. The number of major deals over 100 million euros rose from one to six, generating a total of 910 million euros. The top 5 deals accounted for 50 percent of the volume. The living segment dominated with around 31 percent, while logistics and office properties accounted for around 26 percent and 23 percent respectively.

Alexander von Bülow, Branch Manager JLL Hamburg: “The year started promisingly with some imminent transactions. However, the uncertainties in the Middle East then caused a noticeable cooling of the investment and rental markets. We assume that the Hamburg market will also recover in the second half of the year as the geopolitical situation calms down.”

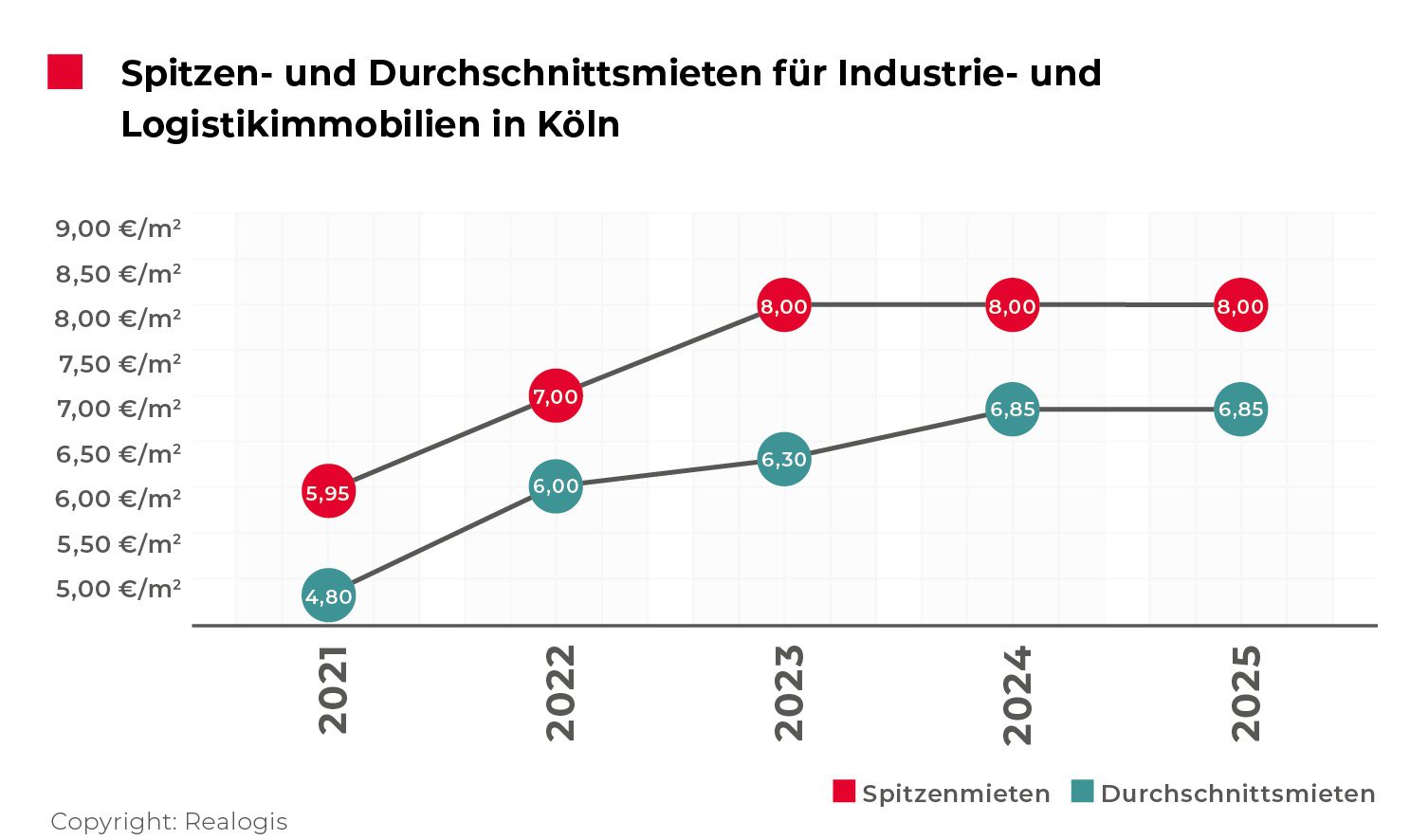

Cologne achieved a transaction volume of 370 million euros, an increase of about 42 percent compared to the previous year, but 49 percent below the ten-year average. The prime office yield rose to 4.6 percent, retail remained at 3.7 percent, logistics at 4.6 percent. German investors were dominant with over 74 percent, while foreign players built up a net of 28 million euros. The top 5 deals represented two-thirds of the volume. Real estate transactions accounted for the largest share at around 35 percent, followed by office and logistics properties at around 33 percent and 15 percent respectively.

Knut Kirchhoff, Branch Manager JLL Cologne: “Overall, Cologne is currently showing very high market activity. Various sales processes from opportunistic to core are currently in the process of being sold, which are expected to lead to a significant increase in transaction volume in the second half of the year.”

At 1.17 billion euros, Munich recorded an increase in sales of 18 percent compared to the previous year, but a decline of half compared to the ten-year average. The prime office yield rose to 4.15 percent, retail stabilized at 3.2 percent, logistics at 4.5 percent. Foreign investors reduced stocks of 145 million euros net. Three major deals worth 100 million euros totalled 520 million euros, which corresponds to 44 percent of the total volume. German buyers dominated with 81 percent. Office properties accounted for around 47 per cent of the volume, while mixed-use properties contributed 15 per cent and residential and logistics properties around 13 per cent each.

Fritz Maier-Hartmann, Branch Manager Munich & Nuremberg: “At around 550 million euros, the office share accounted for around 50 percent of the total investment volume. This shows that the Munich office market is still seen as a safe and attractive investment location despite the tense geopolitical situation. In addition, there is a high level of activity from private investors, and institutional core capital remains quiet.

Several large-volume properties are currently in the process of being sold, so it can be assumed that the transaction volume will remain stable in 2026.

Foreign investors are also becoming more intensively involved with the Munich market again. The focus of prospective buyers is almost exclusively on core locations. It is also evident that the willingness to sell is increasing among the owners. As a result, we expect further price adjustments for properties, especially outside the core locations.”

Stuttgart brings up the rear among the seven metropolises with 180 million euros. The investment volume corresponds to a decline of 47 percent compared to the previous year and 74 percent compared to the ten-year average. The prime office yield climbed to 4.35 percent, retail remained at 3.7 percent, logistics at 4.6 percent. Foreign investors reduced stocks of 38 million euros net. The five largest deals accounted for 83 percent of the volume. German buyers dominated with 79 percent. Office properties were the dominant type of use with around 38 percent, followed by retail properties and the living segment with around 31 and 20 percent respectively.

Georg Charlier, Branch Manager JLL Stuttgart: “As expected, the transaction volume in the first half of 2026 was low and therefore does not come as a surprise. The increased uncertainty caused by the outbreak of the war in the Gulf region has delayed ongoing transaction processes in some cases. Mathematically, these will fall into the result of the second half of the year. In addition, the supply side of the market has grown, which will lead to a further revival of the transaction market. Larger transaction volumes are currently being tested, which is a positive sign for the market.”