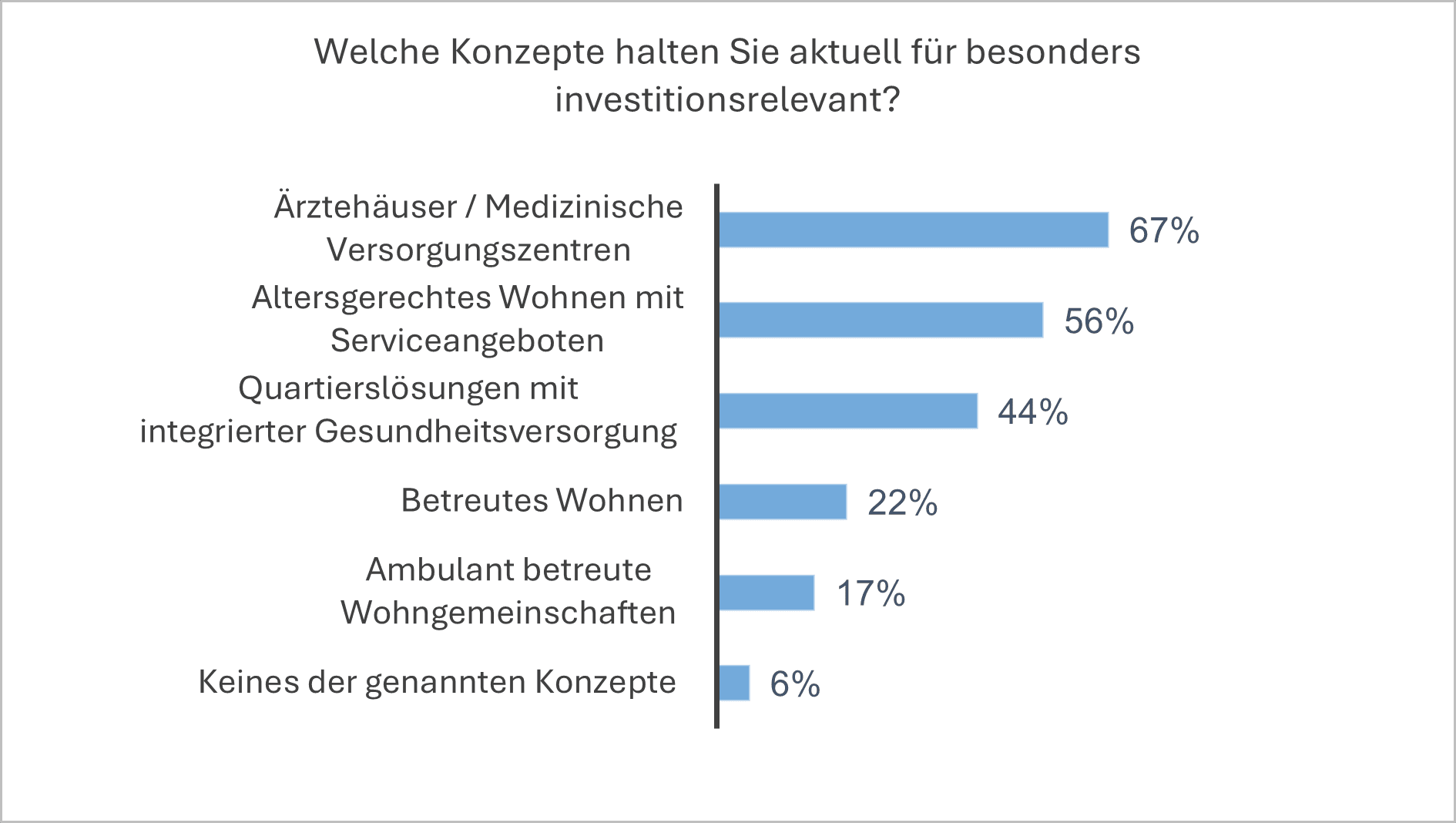

(Berlin) – Hines, a global real estate investment manager, currently rates first-class office properties in Europe as “Strong Buy”. In its research report published today, the company identifies what it sees as an attractive investment opportunity, driven in particular by limited supply and above-average rental momentum compared to other asset classes.

According to Hines’ study “The European Prime Office Rebound”, prime rents in the weighted EU-15 index have risen by 35.6% since the fourth quarter of 2019, representing annual growth of 7.1% (CBRE, Q4 2025). At the same time, construction activity is declining sharply: the number of project starts in the office segment has slumped by 80 percent since its recent peak (RCA, Q4 2025) – more than in any other sector. Against this background, it can be assumed that the limited supply will remain in place in the coming years.

At the same time, demand has changed structurally as a result of hybrid working models. While the overall demand for space has fallen, demand is increasingly concentrated on high-quality, centrally located office space. This development leads to a clear division of the market: first-class properties (Grade A) benefit from stable fundamentals, while secondary portfolios are coming under increasing pressure.

Hines observes that tenant demand is increasingly concentrated in a limited circle of high-quality properties. Due to pricing, the supply gap and rental growth, the company sees good prerequisites for entering the “buying phase” of the cycle in a targeted manner – with a focus on high-performance properties in established and well-connected sub-markets. At the same time, a disciplined approach to risk remains central to ensuring stable returns and long-term portfolio stability.

“The investment environment in the European office market is currently very selective. There is great potential on the German market, especially in the A-locations for modern, sustainable and user-oriented trophy office properties,” says Alexander Möll, Head of Northern & Central Europe at Hines.

Four key drivers of current market development

Vacancy rates in the premium segment have been low for years. New buildings under five years old account for less than 3 per cent of the stock in key sub-markets such as Düsseldorf’s CBD or Amsterdam’s Zuidas and London’s West End. In London’s Mayfair, prime rents have even risen by around 90 percent in the past five years.

In relation to corporate profits, there is still potential for rent increases. In real terms, the burden on users has remained moderate as many companies have reduced their space. In Warsaw and Copenhagen, the rent burden is still relatively low in relation to corporate profit; rising rents appear sustainable, which can make both cities attractive for investment. Warsaw even shows a slightly higher growth potential in direct comparison to Copenhagen.

Well-connected sub-markets offer comparable rental dynamics at significantly lower prices. For example, rents at Frankfurt Central Station are around 23 percent below the CBD level, and space near London Kings Cross is about 37 percent below the West End. The catch-up potential is estimated to be significant.

Rising transaction volumes in core markets such as London’s West End and Paris CBD, as well as positive developments in cities such as Milan, Amsterdam and Munich, point to a gradual return of investor confidence.

In Germany, Hines is currently developing the “B’Ella Berlin” project. The mixed-use quarter with around 67,800 square meters in Berlin-Schöneberg is designed for fossil-free operation and is expected to be completed in the first quarter of 2029. There is currently a pre-letting rate of around 30% for office space.