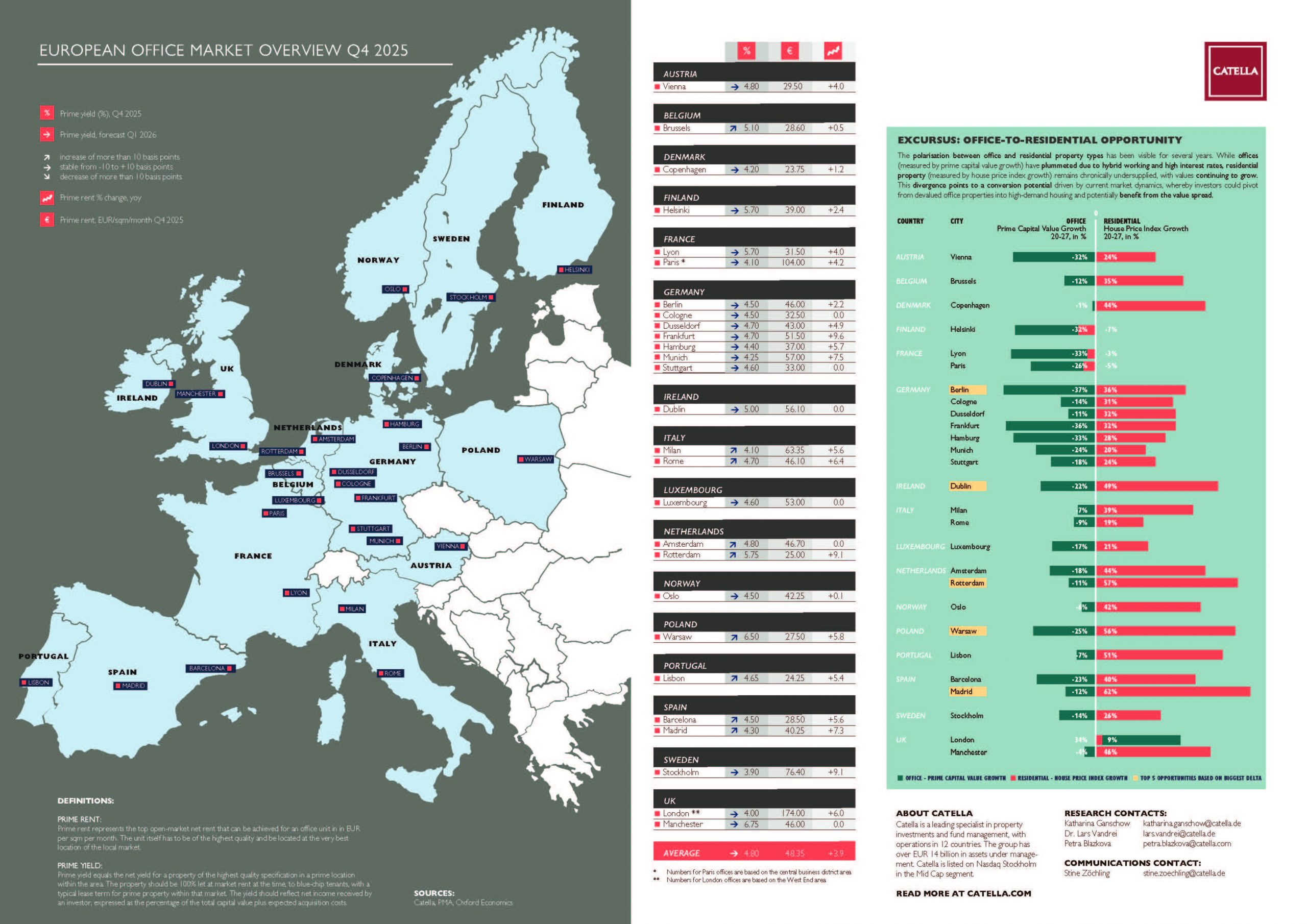

The German investment market for industrial real estate recorded a one-fifth increase in turnover in 2024 compared to the previous year

- Transaction volume: The German investment market for industrial real estate recorded a turnover of around EUR 6.9 billion in 2024, which represents an increase of one fifth compared to the previous year.

- Prime yields: Prime yields remained stable at 4.4% and could fall somewhat in the future.

- Outlook: Although demand for space and rental growth are weakening, demand on the investment market is likely to remain high.

For almost three years now, the ifo business climate index for the manufacturing sector has remained in negative territory. That for retail even for more than three and a half years and in view of the overall weak economic environment, the outlook remains mixed at best. In this environment, the industrial and logistics real estate market* is proving to be remarkably robust. The transaction volume on the investment market amounted to approx. 6.9 billion euros last year. Compared to 2023, this represents an increase of about one fifth, which also narrowly missed the 10-year average of 7.0 billion euros. In addition, turnover was significantly higher than for retail or office properties, the other two major commercial real estate segments. Commenting on these figures, Panajotis Aspiotis, Managing Director and Chief Commercial Officer at Savills, said: “Despite the difficult real and financial environment, investors’ appetite for industrial and logistics real estate is high and the transaction trough brought about by the interest rate turnaround has definitely been overcome. The sector is certainly benefiting from the fact that the environment is even more difficult for other uses, so investors tend to want to increase the industrial real estate quota in their portfolios. This should continue to support demand.”

Lively final quarter and many large-volume sales

Until early autumn, the investment market developed stably, but not very vigorously. This changed in the final quarter of last year: A transaction volume of 2.7 billion euros means by far the strongest quarter in terms of sales since Q1 2022. This was due in no small part to transactions in the three-digit million euro range, which also played a major role for the year as a whole. In total, Savills has registered more than twenty transactions of this magnitude, significantly more than any other usage class. Bertrand Ehm, Director Investment at Savills, adds: “The industrial and logistics real estate segment is currently the only one of the commercial asset classes that is fully liquid even beyond a transaction volume of one hundred million euros. Many large capital collectors have returned to the market after a temporary abstinence and are also ensuring sufficient demand in this volume segment.” Against this backdrop, prime yields have recently remained stable at 4.4%, but could fall somewhat in the future.

Outlook: Continued momentum in the investment market despite weaker rental market

According to Savills, the investment market is likely to continue its upswing in the current year, although the environment on the user markets is tending to deteriorate somewhat. “Although take-up in the logistics segment has been declining since its peak in 2021/22, rents have risen practically across the board until recently. However, the momentum has slowed significantly and this development is likely to continue. Nevertheless, the market remains predominantly a landlord market and we assume that investor appetite will remain greater than concerns about the German economy in the current year,” said Ehm.

* Logistics properties, production properties and business parks