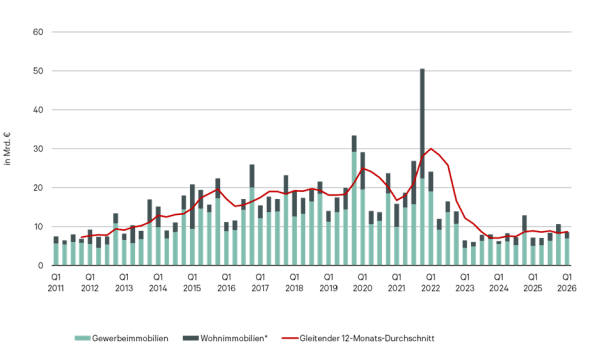

For Germany’s most important office strongholds Berlin, Düsseldorf, Essen, Frankfurt, Hamburg, Cologne, Leipzig and Munich, take-up of 1.3 million m² was recorded at the end of the first half of the year. This means that the market as a whole is moving sideways. In a market environment that remains challenging, Berlin and Munich once again take the lead. The increase in sales here amounts to 51% and 38% respectively in a direct year-on-year comparison. This is the result of the analysis by BNP Paribas Real Estate.

The most important results at a glance:

- Take-up of 1.3 million m² (-5% compared to H1 2025)

- Vacancy volume at 9.1 million m² (+9% compared to H1 2025)

- Construction volume continues to decline to 2.2 million m² (-10% compared to H1 2025)

- Rent levels continue to rise – prime rent in Frankfurt now at €57.00/m²

“The German office markets are convincing in the first half of the year with a sideways movement. In view of the continued weak economic momentum and the additional burdensome conditions since the outbreak of the Iran war, the registered take-up of 1.3 million m² and thus the achievement of the previous year’s level can be regarded as a success. The markets are proving their resilience. The basic dynamic is intact. Driven by significant major deals, take-up in Berlin, Düsseldorf, Frankfurt and Munich has recently even increased,” explains Marcus Zorn, CEO of BNP Paribas Real Estate Germany.

Berlin and Munich are by far the markets with the highest turnover

The Berlin office market is making an impressive comeback. With take-up of 373,000 m² and a take-up increase of 51% compared to the previous year, the German capital is back at the top of the most important office markets. The current half-year result, which is almost 10% above the long-term average, was due in particular to the increased number of major deals. The public administration stands out with two degrees in self-interest. The Federal Ministry for Economic Cooperation and Development will be expanded by 31,500 m², and the Berlin city cleaning service will move into a good 16,000 m². The signing of JetBrains’ lease agreement for 18,500 m² is also a signal. The software provider is thus sending a clear signal for Berlin as an ICT location. A total of four contracts for 10,000 m² of rental space are registered for the federal capital in the first half of the year. All of them with new-build first-occupancy quality, which impressively underlines the focus on demand for top space, especially in the case of large contracts. In Munich, too, four major contracts made a decisive contribution to the significant increase in take-up. At 354,000 m², the previous year’s result was equalled by 38%. The market is thus back in line with the long-term average. As in Berlin, there are four major contracts that are of significant importance, including the new Apple building (for its own use) with around 29,000 m².

The Hamburg and Frankfurt office markets follow at a long distance, with take-up of 177,000 m² and 173,000 m² respectively. Leasing activity in both markets is quite buoyant in the important mid-range segment, but in the current year there are still no major contracts that make the difference in the current market environment. The Düsseldorf market is on track, confirming its previous year’s result with 99,000 m² and registering a contract beyond the 10,000 m² mark for the first time since 2023. KPMG has opted for the One Plaza project and will move into around 17,000 m² there. The Cologne market lacks momentum across the board. The brisk letting activity in the small space segment cannot compensate for the weak closing momentum in the medium and larger segments, so that take-up in the first half of the year amounted to only 76,000 m². The interim results are also disappointing in Leipzig (33,000 m²) and Essen (18,000 m²).

Vacancy rate quoted at 9.1 million m²

The vacancy rate in the office strongholds analysed amounts to a total of 9.1 million m² and is thus 9% above the previous year’s level. The slower pace of growth already registered in the first quarter was confirmed in the second quarter. The latest figures suggest that the cyclical peak has been reached in the office strongholds of Munich, Frankfurt, Hamburg, Düsseldorf and Essen.

The vacancy rate is below 7% in Leipzig (6.1%) and Hamburg (6.5%). Single-digit rates continue to be registered for Cologne (7.0%), Munich (8.0%), Essen (8.5%) and Berlin (9.6%). Vacancy rates remain high in Frankfurt (11.8%) and Düsseldorf (12.4%).

The differentiation of the office market with a clear focus on demand for premium or at least modern space in very well-connected locations is progressing. At the halfway point of the year, the short-term volume of first-time occupancy space in premium locations in the office markets analysed amounts to only 71,400 m². The excess demand remains striking. In Berlin, Düsseldorf, Essen and Cologne, the vacancy rate in the top segment remains well below the 5,000 m² mark. Large-volume space searches in the absolute premium segment can still only be realised within the framework of project developments.

Low construction activity combined with a high pre-letting rate

In the second quarter, the slight decline in construction activity continued in most cities. Only in Berlin and Hamburg were new construction projects started. In the other markets, construction volumes fell or are moving sideways at the previous quarter’s level. In total, around 2.2 million m² of office space is under construction by mid-2026. Compared to the previous year, this corresponds to a decrease of around 10%.

The volume of projected space continues to decline and amounts to a total of only 8.3 million m² in the markets analysed. Compared to the previous year, a decrease of 10% is registered.

Due to the general shortage of high-quality available office space, pre-letting rates remain high or continue to rise in almost all markets. The average pre-letting rate currently stands at 43%, underlining the continued high demand for new-build developments and the rapid pace at which these spaces are being absorbed by the market. In the federal capital, the pre-letting rate is gradually increasing and is now at 23%. For most markets, odds well above 50% are registered. Leipzig (just under 82%) and Cologne (just over 74%) report top values.

The available space relevant to the office market – consisting of vacant space and space still available in construction projects – amounted to 10.3 million m² at the end of June 2026. Compared to the same period last year, this corresponds to a moderate increase of 6%.

Prime rent in Frankfurt now at €57.00/m² – rent levels continue to rise

The persistently low availability of high-quality office space in prime locations and the concentration of large space searches on new construction projects in the premium segment continue to put upward pressure on prime rents. As a result, the prime rent in Frankfurt rose by €2.00/m² to €57.00/m² (+4%) in the second quarter. In the other cities considered, prime rents remained at the high level of the previous quarter. Munich remains the most expensive location at €59.50/m². For Berlin (€47.00/m²) and Düsseldorf (€46.00/m²), values above the €40 mark are each reached. Below this are Hamburg (€39.00/m²), Cologne (€33.50/m²), Leipzig (€21.00/m²) and Essen (€20.00/m²).

The general demand focus on modern and ESG-compliant office space is reflected in the development of average rents. Across all locations, the average rent rose by a good 3% to €22.20/m² over the course of the year. In a direct quarter-on-quarter comparison, Düsseldorf (+4.5% to €23.00/m²), Frankfurt (+3.7% to €28.30/m²), Essen (+0.7% to €13.90/m²) and Berlin (+8.5% to €29.30/m²) continued to rise. In no other city is the average rent level higher than in the Spree metropolis. The average rent is stable or with temporary minimal declines in Leipzig (€13.50/m²), Cologne (€20.90/m²), Hamburg (€21.90/m²) and Munich (€27.00/m²).

Prospects

For the time being, the development on the German office markets will continue to be influenced by geopolitical uncertainties and a weak economy. For the moment, the renewed rise in interest rates, which makes future-oriented company expansions more difficult, as well as the transformation process taking place across the German economy, in which the integration of AI into the world of work is likely to play a role that should not be underestimated, are having a negative impact on the moment.

With the reform package now presented, the German government has taken a first step towards promoting future viability and growth in the state. Relief, flexibilisation and reduction of bureaucracy can provide positive impetus in the medium to long term and thus stimulate demand for office space in the long term. The potential that regions and companies can have is already demonstrated by economically strong regions such as the Munich Metropolitan Region with its strong technology sector, as well as innovations in robotics that are attracting worldwide attention.

“The basic dynamics in the German office market will not change much in the short term. We expect continued brisk leasing activity in the small and medium-sized space segment, while major deals will continue to take longer to initiate, but will then come. The demand focus on modern, ESG-compliant space remains and will manifest itself in large contracts in particular. In view of the continuing decline in the pipeline of new construction and the glaring shortage of space with first-occupancy quality, the pressure on the rent level and especially on prime rents remains. The vacancy rate is reaching its peak, although renovation and conversion will remain an issue for owners of outdated and no longer marketable existing buildings,” explains Marcus Zorn, summing up: “With more courage, planning security and deregulation, the German economy should be somewhat more dynamic again towards the end of the year, with a positive influence on office space take-up. For the year as a whole, we consider take-up to be slightly above the previous year’s level to be realistic.”