BNP Paribas Real Estate publishes investment figures for Q1 2025

The increase in investment turnover in Germany not only continued in the first quarter of 2025, but even accelerated slightly. With a total result of just over €8.4 billion, the transaction volume increased by a good third compared to the previous year. Particularly noteworthy is the development of residential investments (from 30 units), which have more than tripled and contribute a good € 2.5 billion to sales. As a result, they also account for the largest share of the overall result at just under 30%. The transaction volume with commercial real estate in the first quarter of 2025 amounted to a good €5.9 billion. Although the increase in sales in this market segment is noticeably lower at around 7%, it basically confirms the upward trend that was already evident at the end of last year. This is shown by the latest analysis by BNP Paribas Real Estate.

The most important results at a glance:

- At just over €8.4 billion, investment turnover was 34% higher than the previous year’s figure

- Of this figure, more than €2.5 billion (+227%) is attributable to the Residential market segment

- Commercial investments account for a good €5.9 billion (+7%)

- 77% (€4.6 billion) of commercial sales are accounted for by individual deals

- Portfolio sales totalled €1.4 billion

- In the commercial market segment, office investments are at the top with just under €1.8 billion, ahead of logistics and retail investments with just under €1.3 billion each

- At the beginning of 2025, Berlin will again be the number 1 German A-location (€986 million)

- Net prime yields were stable at the beginning of the year

- At 36%, the market share of foreign investors is roughly on a par with the previous year

- Around 340 transactions recorded

“The very significant market recovery in the residential segment underlines that the medium and long-term prospects of the German housing markets are positive from an investor’s point of view. Due to the still too low volume of new construction, considerable excess demand can be expected in the coming years, which is likely to be reflected in further increases in rents. For investors, this results in attractive future value appreciation potential, which makes residential investments very interesting,” explains Marcus Zorn, CEO of BNP Paribas Real Estate Germany. Against this background, investors were also prepared to accept moderate purchase price increases in the high-quality new-build segment in recent months. Even the slight increase in financing costs in recent weeks in the wake of the announced special fund has so far had little effect on the fundamentally upward sentiment on the buyer side. This is also supported by the fact that a noticeable market revival was observed not only in the new construction sector, but also in the existing segment with a value-add profile.

Commercial investment turnover also continued to increase slightly in the first quarter

“The transaction volume in commercial real estate in the first three months of the year amounted to a good €5.9 billion, which is around 7% higher than the comparable figure for the previous year. Although the increase in sales is considerably lower than in the residential sector, it nevertheless underlines the slight upward trend that has been observed in principle for some time. This still positive development is quite remarkable, as current market events are influenced by very different factors. These include the persistently weak GDP forecasts for this year and next, which do not point to a major economic recovery. And the uncertainty about the effects and, above all, the sustainability of the tariff increases on the part of the US government is also contributing significantly to the uncertainty of the economy,” says Marcus Zorn. “At the same time, however, the announcement of the special fund worth several hundred billion euros for infrastructure and environmental protection measures as well as the creation of considerable financial leeway for defence spending has nourished the hope that the German economy could benefit significantly from this. This is reflected not least in the positive development of the ifo business climate index, which has now risen three times in a row to 86.7 points in March. Above all, expectations have risen noticeably, which suggests that many companies are hoping for a significant improvement. Last but not least, the user markets would also benefit from an overall improvement in economic development and contribute to higher demand for space. This should also further strengthen the willingness to invest in real estate,” explains Marcus Zorn.

“The increase in financing costs observed in recent weeks in the wake of increased swap rates and the higher yields on German government bonds are likely to postpone the yield compression expected for this year until recently for the time being, but they will do little to change the fundamentally higher willingness to invest in real estate. The current significant increase in supply and the high willingness to sell on the part of owners will also continue to support the emerging market recovery in the coming quarters,” adds Nico Keller, Deputy CEO of BNP Paribas Real Estate Germany.

Office properties regain their top position

Looking only at commercial investments, office properties were able to regain their traditional top position, which they had lost in logistics properties in the last two years, in the first quarter of 2025. With a transaction volume of just under €1.75 billion, they have doubled their previous year’s result and, at almost 30%, contribute the most to commercial investment turnover. Significantly impacted by the sale of the Upper West in Berlin with well over €400 million. But even without this benchmark transaction, offices would have secured first place. This is due on the one hand to an increased number of office sales, but also to a noticeable increase in the average deal volume from a good € 17 million (Q1 2024) to currently around € 30 million per sale. A number of transactions were registered, especially in the mid-market segment between €25 million and €100 million. This shows that investors are increasingly regaining confidence in the medium and long-term development of the German office markets. This was also due in part to the user markets, which recorded a noticeable recovery trend in the first quarter with a plus of 16%.

Logistics and retail investments follow almost equally in second and third place with almost €1.3 billion each, so that both types of use each achieve a market share of just under 22% of commercial investment turnover. For logistics properties, which amount to just over €1.29 billion, this result corresponds to a moderate decline of around 8%. This is mainly due to the noticeable decline in volume in the portfolio segment, whereas almost €1.1 billion was generated from individual transactions, which corresponds to the fourth-best result ever recorded at the start of the year. It is particularly noteworthy that sales were achieved in the three-digit million range without a single sale. In contrast, market activity has increased, especially in the mid-market segment, which is also reflected in the number of deals recorded, which increased by 14%.

The decline was more extensive in the retail segment, where earnings of €1.28 billion are currently around 35% below the comparable prior-year figure. However, it should be noted that an exceptionally strong result was also achieved in the first quarter of 2024. One of the largest deals at the beginning of 2025 was the sale of the B5 Outlet Center in Wustermark for over €200 million. Specialists and supermarkets were once again particularly popular with investors, contributing around €831 million to retail property take-up, which corresponds to a share of almost 65%. Inner-city commercial buildings accounted for a further €135 million, or almost 11% of all retail investments.

Fourth place is occupied by healthcare properties with a volume of € 580 million, which corresponds to an increase of 144%. However, this asset class is still a long way from the high turnover of 2020-2022. Revenue from hotels remained almost unchanged, at €238 million, almost exactly at the previous year’s level. The generally significant increase in interest of many investors is not yet reflected in the transaction volumes recorded in the first quarter of 2025.

Portfolio sales in particular recorded a significant increase in sales

Although both individual and portfolio transactions were able to increase their turnover, the increase in individual properties was comparatively moderate at just under 4%. Parcel sales recorded noticeably higher growth, with transaction volume increasing by almost 19%. Their share of total commercial real estate turnover thus amounts to 23%, the highest share of the last three years. By far the most investments were made in retail portfolios at €682 million, followed by healthcare deals at €380 million and logistics packages at €208 million. In contrast, no portfolio transactions with office or hotel properties were registered in the first quarter of the year.

At 36%, the share of foreign investors in total commercial real estate turnover is roughly at the same level as in the previous year. In a long-term comparison, this also achieves a comparable order of magnitude as in the first quarters of the last ten years. As expected, European investors contributed the highest shares of total commercial sales with just under 19%, followed by North American buyers with just under 15%.

A locations roughly at the previous year’s level

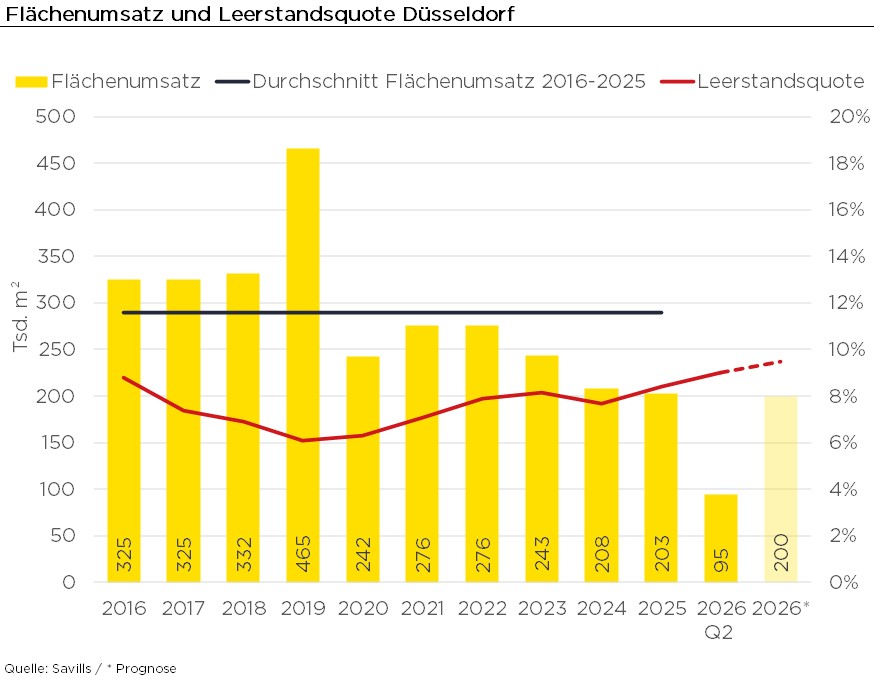

“The transaction volume in the German A locations (Berlin, Düsseldorf, Frankfurt, Hamburg, Cologne, Munich, Stuttgart) amounted to around €2.52 billion in the first three months and is thus lower (-10%) than in the same period of the previous year. In general, the market activity in the large cities has become somewhat livelier, but at the same time there are still relatively few large-scale deals. So far, only three sales in the three-digit million range have been made. Against this background, different developments can be observed within the individual cities,” explains Nico Keller. Berlin is by far in first place with a result of €986 million, which corresponds to an increase of 115%. The sale of the Upper West to the Schoeller Group’s family office made a significant contribution to this. Munich is in second place with €508 million. Unlike in the capital, however, the result here is about 60% below the previous year’s figure. In the Bavarian capital, only one major deal in the lower three-digit million range could be counted, whereas the previous year’s figure was significantly influenced by the sale of the 5 farms for € 700 million. Hamburg also made it onto the podium, where €456 million was invested, which corresponds to an increase of a good 21%. This was mainly due to the sale of 13 nursing homes owned by Deutsche Wohnen to the City of Hamburg. Düsseldorf follows in second place with €249 million (-23%), Cologne with €87 million (-40%) and Stuttgart with €71 million (+16%).

Yields stable in the first quarter of 2025

After almost all market participants assumed at the end of last year that the first yield compressions could be expected in the course of 2025, the situation has currently changed considerably. This is due to increased financing costs in recent weeks, higher yields on German government bonds and key interest rate decisions by the major central banks that are currently difficult to calculate due to the expected effects of the US tariff increases. As a result, yields are unchanged at the beginning of the year. The net prime yields for offices are 4.36% on average in A-locations. Munich remains the most expensive location with 4.20%. It is followed by Berlin and Hamburg with 4.25%. In Cologne and Stuttgart, 4.40% are quoted and in Frankfurt and Düsseldorf 4.50% are to be estimated. For logistics properties, the prime yield is 4.25%, and for commercial buildings, the average for A-locations is 3.76%. No changes were observed in retail parks (4.65%), discounters/supermarkets (4.90%) and shopping centres (5.60%) either. In the housing market, the prime yield for new-build properties remains at an average of 3.58% in large locations.

Prospects

The further development of the investment markets is subject to very different influencing factors and will have to face an extremely heterogeneous environment, in which there is also the risk that it could change fundamentally several times and in the short term. Expected effects result from both national and international developments and contexts, the severity of which is hardly predictable. On the one hand, there are the major risks for the entire global economy resulting from the announced tariffs by the USA and carrying the potential for a full-blown trade war. If the worst-case scenario were to materialise, this could have devastating consequences for the further economic development of many countries. On the other hand, the special fund that has been decided upon, in conjunction with the greater financial leeway for defence spending, is available to Germany in particular as an instrument for additional growth impulses, so that GDP growth in the next few years is likely to be somewhat higher than previously forecast. Due to extensive secondary effects, this would also stimulate user markets, which should further improve the framework conditions for real estate investments. It is not possible to predict which of the risks and opportunities outlined above will ultimately have a greater impact on the markets. Not least because there is a great deal of uncertainty as to how sustainable political decisions will be and whether another change of course might not completely change the investment environment again.

Another influencing factor is the financing conditions. Swap rates that have risen in recent weeks, but also higher yields on German government bonds, do not currently indicate price increases and thus falling yields. However, short-term changes in the wake of the announcement of certain measures and/or packages should not be overestimated, as it remains to be seen whether the adjustments are truly sustainable. Another important aspect is the looming inflation trend. Inflation is likely to pick up again in large parts of the world in the course of the year. Against this background, the probability that the major central banks will continue to lower key interest rates is very low. Rather, everything indicates that financing is likely to become little or not at all cheaper in the further course of the year.

However, real estate investments could also benefit from the outlined mixed situation in connection with the resulting planning uncertainty. Especially in uncertain times with strong fluctuations in the performance of many asset classes, many large investors often focus on broader diversification of their portfolios. As a rule, less volatile asset classes, where real estate is usually in first place, benefit from this. This could indicate a significant increase in interest, especially among international investors, in investing in German real estate.

“The overall view of the outlined influencing parameters shows that forecasts can only be made within the framework of scenarios, as the uncertainty regarding the further development of many important factors is currently too great for more quantitatively substantiated forecasts. In our view, the most likely scenario is to expect an accelerated recovery of the German economy, from which the user markets will benefit. In the course of the increasing demand for space, investments are becoming increasingly attractive. In addition, it is likely that many investors are likely to turn more towards the safe asset class of real estate. As a consequence, the transaction volume should continue to rise moderately over the course of the year. We are sticking to the forecast made at the end of last year that a result of over €40 billion for investments in commercial and residential properties does not seem unrealistic. The situation is different when it comes to yield development. Due to the changed framework conditions, a stable development in the further course of the year is the most likely scenario from today’s perspective,” summarizes Marcus Zorn.